Deeds of Variation vs. Deeds of Disclaimer

A Simple Guide for Beneficiaries in England and Wales

When you inherit from someone’s estate, you may find that the original distribution does not reflect your personal wishes, family circumstances, or financial priorities. In England and Wales, beneficiaries can use two main tools to change what happens to their inheritance.

These two tools are known as a Deed of Variation and a Deed of Disclaimer. Although they may appear similar, they operate quite differently. In this guide we explain each option in straightforward language so that you can easily tell the difference between a Deed of Variation and a Deed of Disclaimer.

What Is a Deed of Variation?

A Deed of Variation allows a beneficiary of an estate to legally redirect all or part of their inheritance to someone else. The Will, or Intestacy Rules if there is no Will, remain unchanged, but the beneficiary alters how their personal share is distributed.

What are the Key Features of a Deed of Variation

- You may redirect all or part of your inheritance to any person or charity

- It must be completed within two years of the date of death for tax efficiency purposes

- Often used for Inheritance Tax (IHT) or Capital Gains Tax (CGT) planning

Common Reasons to Use a Deed of Variation

- To improve tax efficiency within the estate

- To support family members who were left out of the Will

- To correct imbalance or help maintain family harmony

- You want flexibility in how the estate is shared

- You want to reduce tax liability

"*" indicates required fields

What Is a Deed of Disclaimer?

A Deed of Disclaimer allows a beneficiary of an estate to refuse their inheritance entirely. Once you disclaim, you do not receive the asset or funds and cannot decide who gets the inheritance. Instead, the inheritance reverts back to the estate and is distributed under the Will or Intestacy Rules, if there is no Will.

What are the Key Features of a Deed of Disclaimer?

- You must disclaim before accepting the gift

- You must disclaim the whole gift, not part of it

- You have no control over the new recipient

Common Reasons to Use a Deed of Disclaimer

- Avoiding assets that may bring financial or tax complications

- Allowing the estate to pass according to an original Will without your involvement

- You are happy for the Will or Intestacy Rules to determine who benefits from the inheritance

Can I Vary a Will After Someone Has Died?

Yes, it is possible to vary a Will after someone has died, and there are legal provisions that allow for this. This process is typically done using a Deed of Variation, which gives beneficiaries the ability to alter how the estate is distributed, even after the death of the individual who made the Will. Read more…

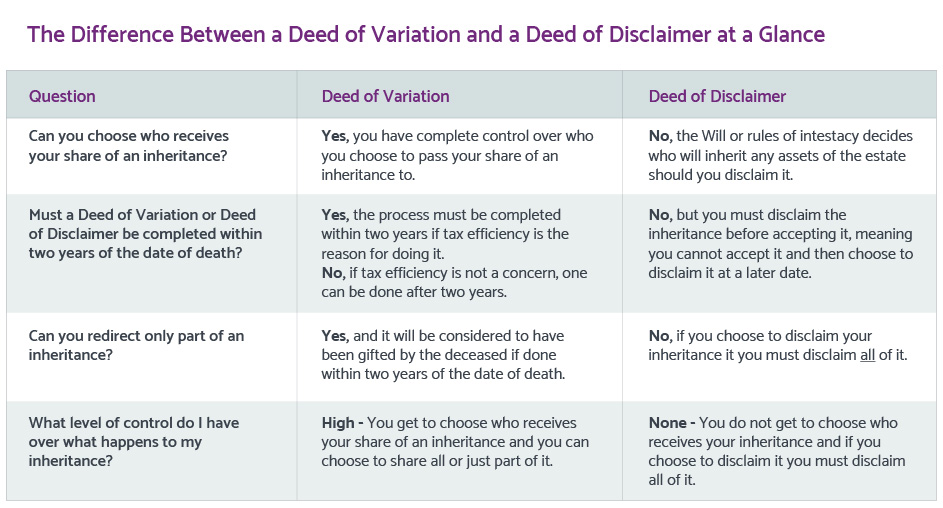

What are the Key Differences Between a Deed of Variation and Deed of Disclaimer?

There are some key differences between a Deed of Variation and a Deed of Disclaimer which are important to be aware of. The table below summarises the key differences and will help you identify the right solution for you and your situation. If you need further help understanding the difference and deciding which is the right option for you, you can call us on 01924 290 029 or contact us using our online enquiry form.

Contact our specialist Deed of Variation Solicitors today for Advice

At Thornton Jones Solicitors, our experienced private client team can guide you through every step of putting a Deed of Variation or Deed of Disclaimer in place by:

- Explaining the key differences between a Deed of Variation and a Deed of Disclaimer, and which option best suits your circumstances

- Advising on the legal and tax implications, including Inheritance Tax (IHT) and Capital Gains Tax (CGT) considerations

- Helping you understand your rights as a beneficiary and the level of control each option provides

- Preparing the legal documentation accurately and in compliance with all formal requirements

- Ensuring any Deed of Variation is completed within the relevant two-year timeframe for tax purposes

- Liaising with personal representatives and other beneficiaries where required

Deciding what to do with an inheritance is an important financial and personal decision. Whether you wish to redirect your entitlement or formally refuse it, obtaining the right legal advice ensures your interests are protected and the process is handled correctly.

Get in touch with our friendly and knowledgeable team today to discuss your options. You can call us on 01924 290 029 or contact us using our online enquiry form.

Deed of Variation and Deed of Disclaimer FAQs

While a solicitor is not legally required for either document, professional advice is strongly recommended. A Deed of Variation must contain specific tax statements and meet formal requirements to be valid, and both documents may have long-term financial consequences.

Yes. A Deed of Variation can be completed before or after a Grant of Probate or Letters of Administration, as long as it is within two years of the date of death for tax purposes.

No. A Disclaimer is a complete refusal of the gift, and you cannot control who receives it next. The estate is distributed according to the Will or Intestacy Rules as if you had died before the deceased.

Generally, no. Once a Disclaimer is validly made, especially once the personal representative(s) act on it, it is effectively final. Beneficiaries should seek advice before signing because Disclaimers cannot simply be revoked.

Yes. When completed within two years of death and containing the correct tax statements, a Variation can allow assets to be redirected in a more tax‑efficient way. This can help reduce Inheritance Tax or Capital Gains Tax exposure in some circumstances.

Yes. A Deed of Variation can involve multiple beneficiaries if more than one person wishes to redirect their inheritance. Each person only affects their own share, unless the changes impact others who must then consent.

A Disclaimer applies to the entire gift, whether assets or debts or liabilities are attached. If the inheritance involves responsibility you do not wish to take on, a Disclaimer may be appropriate, but take legal advice, as it may have unintended legal consequences.

The content of this blog post is for information only and does not constitute formal legal advice and should not be relied upon as advice. Thornton Jones Solicitors Limited accepts no liability for any such reliance upon this content. Where the post includes links to external websites, Thornton Jones Solicitors Limited accepts no responsibility for the content of such sites. Any link to a third-party website should not be construed as endorsement by Thornton Jones Solicitors Limited of any content, products or services which are outside our direct control.

Deed of Variation Solicitors

NS&I Bereavement Claims Error – Where has it all gone wrong?

NS&I is one of the largest savings organisations within the UK, and therefore the recent headlines of “missing savings” and “prizes withheld” are alarming for everyone, not least the bereaved families whose loved ones held accounts with government-backed NS&I.

What is NS&I?

Originally established as the Post Office Savings Bank, National Savings & Investments (NS&I) is a government-owned savings provider in the UK, best known for its Premium Bonds product. Rather than paying interest, Premium Bonds offer entry into monthly prize draws, with two £1 million prizes and a range of smaller awards.

What other types of savings products do NS&I offer?

NS&I also offers other savings products, including ISAs and Income Bonds, the latter providing monthly interest payments. All funds held with NS&I are backed by HM Treasury, meaning savers benefit from a government guarantee, offering greater protection than that typically available through banks and building societies.

With no high street branches, NS&I are only contactable remotely. Money earned from NS&I customers and through its savings accounts and bonds offerings are used to fund public spending, and all deposits are backed by the UK Government with no upper limit, unlike the FSCS offered by the majority of high street banks.

How Does an NS&I Bereavement Claim Work?

When someone dies, their executors (if there is a Will) or personal representatives (if there is not) are responsible for notifying NS&I of the death, usually by providing a death certificate and relevant estate details.

Once notified, NS&I will carry out checks to identify any accounts or investments held by the deceased, including Premium Bonds, savings certificates, ISAs and Income Bonds. This step is intended to ensure that all holdings are correctly located, even where accounts may have been opened many years earlier.

NS&I will then provide instructions on how the accounts can be closed and the funds released. This typically involves completing bereavement claim forms and supplying evidence of authority to act on behalf of the estate.

Is Probate always required?

Whether probate is required will depend on the value of the NS&I holdings and the wider estate. Smaller balances may be released without probate, whereas larger estates will usually require a grant of probate (or letters of administration) before funds can be encashed and distributed to beneficiaries.

An executor is the person (or people) appointed in a Will to deal with the administration of the deceased’s estate after their death. Their role is to ensure that the deceased’s wishes, as set out in the Will, are carried out properly.

This typically includes identifying and collecting assets, settling any debts and liabilities, dealing with tax affairs, and distributing the remaining estate to the beneficiaries named in the Will. Executors may also be required to apply for a grant of probate, which provides them with the legal authority to deal with certain assets, such as bank accounts or investments.

Executors carry significant legal responsibility and must act in the best interests of the estate and its beneficiaries throughout the administration process.

Personal representatives is the legal term used to describe the individuals responsible for administering a deceased person’s estate. This includes executors where there is a valid Will, or administrators where there is no Will (intestacy).

In practical terms, personal representatives carry out the same core duties: identifying and valuing the estate, collecting assets, paying any debts and taxes, and distributing the estate to the rightful beneficiaries. Where a Will exists, the named executors automatically become the personal representatives once probate is granted.

They are legally responsible for ensuring the estate is administered correctly and in accordance with either the Will or the rules of intestacy, depending on the circumstances.

What Has Gone Wrong with NS&I Bereavement Claims?

It has recently been revealed in the news that up to 37,500 bereavement claims have been affected due to NS&I having lost track of investments and withholding premium bond prizes from the families of their deceased customers. That said, work to identify the affected parties is still underway so the true scale of the tracing issue isn’t certain.

Despite this issue only recently making the headlines in March 2026, it has been reported that the problem was initially reported to Government ministers in December 2025.

NS&I have explained that there had been errors in identifying all deceased account holders NS&I accounts, which in turn meant that executors and personal representatives were not always repaid money from all of the deceased’s accounts despite lodging bereavement claims in the correct manner.

What Is Probate?

The word probate is used to describe the process involved in dealing with the administration of a person’s estate when they have died. Probate can also be used to describe the legal document giving authority to the person or persons to administer the deceased’s estate. Read more…

What is NS&I’s Response to Missing Savings and Withheld Premium Bond Prizes?

NS&I have now advised that the identification issue has been resolved and that stringent measures have been put in place to ensure that no such issues happen again. Although this is little comfort for those battling to get their money back.

NS&I have confirmed that most cases affected relate to bereavements from 2008 – 2025, and it is estimated that the money owed from NS&I to the affected deceased estates could be up to £476 million. NS&I have been criticised by the financial ombudsman for repeatedly stating that its figures were accurate and correct, with this insistence only serving to prolong the investigation.

To date, NS&I have hired new staff to assist with making contact with the affected families and they will publish details of how they will reimburse the “missing” funds. As NS&I is government backed, the funds are protected, however it is likely to take some time for NS&I to reconcile the funds with the correct people.

What are the Tax Implications and What Should Affected Families Should Consider?

Where missing NS&I funds are later identified and returned to an estate, this can have knock-on tax consequences that executors and personal representatives will need to consider. Although the recovery of assets is beneficial, it may increase the overall value of the estate and affect its tax position retrospectively.

In particular, inheritance tax (IHT) may need to be reassessed if the additional funds change the estate’s total value. This could result in further tax becoming payable or require amendments to previously submitted IHT accounts to HMRC.

There may also be capital gains tax (CGT) considerations depending on how the estate has been administered, particularly where assets have been sold or invested during the administration period. In addition, any interest or compensation paid alongside the returned funds may itself have tax implications.

Given the complexity, executors may wish to seek professional advice to ensure the estate is correctly reported and any tax liabilities are properly addressed.

"*" indicates required fields

Do You Need to Take Action on an NS&I Bereavement Claim?

NS&I has confirmed that it is working to identify and contact affected estates in relation to the bereavement claims issue and any missing or unallocated savings. Where an estate is impacted, NS&I will contact executors or personal representatives directly with details of any funds due and how these will be returned.

NS&I has also advised that it is not necessary to use claims management companies, as this is unlikely to speed up the process and may result in avoidable costs.

However, executors should still ensure that all NS&I assets have been properly included in the estate administration. Where there is uncertainty or concern about missing funds, legal advice may be helpful to ensure the estate is fully and correctly administered.

Contact our Wills & Probate Solicitors today for Advice

At Thornton Jones Solicitors, our specialist Private Client and Wills & Probate team advises individuals, executors and families dealing with estate administration issues, including complex bereavement claims involving financial institutions such as NS&I.

We can assist you by:

- Advising on your duties as an executor or personal representative

- Helping you trace and identify missing assets within an estate, including NS&I savings and Premium Bonds

- Guiding you through the probate process where required

- Assisting with correspondence and claims to financial institutions

- Advising on delays, discrepancies, or missing funds in estate administration

- Supporting you with any tax considerations arising from delayed or additional estate assets

Dealing with an estate can be complex, particularly where assets are missing, delayed or incorrectly recorded. If you are concerned about NS&I bereavement claims or believe an estate may be owed funds, our team can provide clear, practical legal advice tailored to your circumstances.

To speak to our friendly Wills & Probate team, please call 01924 290 029 or contact us using our online enquiry form.

Wills and Probate Solicitors FAQs

If you believe funds may be missing, you should first ensure that a bereavement claim has been properly submitted to NS&I. If this has already been done, it is advisable to wait for NS&I to contact you, as they have confirmed they are proactively identifying affected cases.

If you remain concerned, executors or personal representatives can contact NS&I directly to request a review of the deceased’s accounts and confirm whether all funds have been accounted for.

NS&I offers a tracing service as part of its bereavement process. Executors or personal representatives can submit details of the deceased, and NS&I will attempt to locate any accounts or investments held in their name.

This is particularly important where paperwork is incomplete or where the deceased held Premium Bonds or older savings products.

Not always. Whether a grant of probate is required depends on the value of the assets held with NS&I. For lower-value holdings, NS&I may release funds without a grant. However, for larger estates, probate is usually required before funds can be encashed and distributed.

NS&I has stated that it is working to identify affected customers and will contact families directly where issues are found. However, given the scale of the problem and the time period involved, executors may wish to be proactive if they suspect something has been missed.

In addition to the return of any missing funds, affected estates may be entitled to interest and, in some cases, compensation. The exact amount will depend on the circumstances, including how long the funds were outstanding and whether there has been any financial loss as a result of the delay.

Yes. Premium Bonds remain eligible for prize draws for a period after death (usually up to 12 months), provided the funds have not yet been encashed. Any prizes won during this time should form part of the deceased’s estate and be payable to the beneficiaries.

Potentially, yes. If additional funds are later identified and returned to the estate, this could impact the overall value of the estate for inheritance tax purposes. This may require the personal representatives to revisit earlier tax calculations and, in some cases, submit corrective information to HMRC.

Not necessarily. NS&I has indicated that families do not need to use claims management companies, and many straightforward cases can be handled by executors directly. However, legal advice may be helpful where there are complications—such as missing funds, tax implications, or disputes between beneficiaries.

There is no fixed timeframe. Given the number of potentially affected cases, it may take some time for NS&I to investigate and reconcile all accounts. Executors should be prepared for delays, particularly in more complex cases or where older accounts are involved.

The content of this blog post is for information only and does not constitute formal legal advice and should not be relied upon as advice. Thornton Jones Solicitors Limited accepts no liability for any such reliance upon this content. Where the post includes links to external websites, Thornton Jones Solicitors Limited accepts no responsibility for the content of such sites. Any link to a third-party website should not be construed as endorsement by Thornton Jones Solicitors Limited of any content, products or services which are outside our direct control.

Wills & Probate Solicitors

Sean Hughes Death: The Dangers of a Homemade Will

The well loved Irish comedian Sean Hughes sadly passed away in 2017, leaving behind an estate of approximately £4 million. This included his main residence, estimated to be worth £1.8 million and two additional properties together estimated to be valued at £2.15 million.

The Problems With a Homemade Will

Sean’s Will was home-made, and it left “my three houses to Shelter” but at the time of his death only one of the three properties was owned in Sean’s personal name. The other two properties were owned by a company of which Sean was the sole shareholder.

Sadly, Sean’s estate is an example of some of the problems that preparing a home-made Will can lead to.

Sean’s estate had to be referred to the Court for a decision on how the estate should pass. Only now, almost 10 years after Sean’s death, has the dispute been concluded.

Why a Home-Made Will Can Be Invalidated Simply Due to the Choice of Wording

The issue with Sean’s choice of wording for the gift of the three houses to Shelter, is that strictly speaking only the one owned in Sean’s personal name was covered by this wording. The two properties owned by the company would fall into the residue of Sean’s estate, as technically they were not “his” houses, they were assets of the company.

The issue for the Court to consider, was whether the company shares (and therefore the properties owned by the company) should pass to Shelter along with the other property which was held in Sean’s personal name.

Fast, Free and Risky: Why You Shouldn’t Use AI to Write Your Will

Artificial intelligence is becoming part of everyday life. From drafting emails to answering questions and generating documents, it can feel quick, convenient and cost-effective. It’s therefore no surprise that some people are considering using AI tools to prepare their Will. Read more…

Sean Hughes left Three Properties to Shelter in his Homemade Will

Sean had been a long term supporter of the charity Shelter, and his family wished that all three properties should pass to Shelter.

The Court agreed that it was Sean’s intention that all three properties were to pass to Shelter and therefore this is what was ordered.

Sean’s family described him as a “great and generous comedian” who was “horrible at admin.” They went on to state that “we hope that Sean’s legacy will encourage others to think of people less privileged when making their final plans (ideally with at least a little bit of legal advice!)”.

What Are the Risks of Making a Homemade Will?

Sean’s case took almost 10 years and significant expense to be concluded, however these cases are becoming more common with the progression of technology and AI making it feel easier than ever to prepare your own Will.

Some of the common problems with homemade/AI made Wills are:

- Partial intestacy, where gifts fail or do not cover all the assets that the testator intended to be covered due to poor or ambiguous wording.

- Complexities of business assets etc not being fully understood and therefore not correctly provided for in the Will.

- Misunderstandings around how different jointly owned assets will pass upon death and when additional steps need to be taken to ensure that joint assets pass how the testator wishes.

- AI cannot accurately assess a person’s capacity or their mental state when they are making their Will, leaving home made Wills more open to challenge than solicitor prepared Wills where stringent records are kept regarding the making of the Will.

"*" indicates required fields

Contact our Wills & Probate Solicitors for Advice

At Thornton Jones we can assist you to prepare a legally valid Will to ensure that your estate passes to those that you wish to benefit. If you would like to make an appointment to discuss this further, please call one of our offices to arrange an initial consultation.

If you need assistance or advice you can contact our team today on 01924 290 029 or contact us using our online enquiry form.

Wills & Probate FAQs

Homemade wills can lead to serious legal issues, including unclear wording, missed assets and partial intestacy. As seen in Sean Hughes’ case, this can result in lengthy court proceedings, delays in distributing the estate and significant legal costs. Thornton Jones say that even well-meaning DIY wills can cause long-term complications. A professionally drafted will ensures your estate is protected and your wishes are clearly followed.

Yes, a will can be challenged if its wording is ambiguous or does not clearly reflect the person’s intentions. Courts may need to interpret the will, which can be time-consuming and expensive, potentially delaying the distribution of the estate. At Thornton Jones Solicitors we often see wills delayed or disputed because key details were overlooked. Seeking professional guidance from an experience and qualified solicitor can prevent unnecessary stress for your loved ones.

A solicitor ensures your will is legally valid, clearly drafted and covers all of your assets, including complex arrangements like business ownership. They also assess capacity and keep detailed records, helping to reduce the risk of disputes or challenges after death. At Thornton Jones, we make sure every will is tailored to the client’s circumstances, providing clarity, security and peace of mind.

The content of this blog post is for information only and does not constitute formal legal advice and should not be relied upon as advice. Thornton Jones Solicitors Limited accepts no liability for any such reliance upon this content. Where the post includes links to external websites, Thornton Jones Solicitors Limited accepts no responsibility for the content of such sites. Any link to a third-party website should not be construed as endorsement by Thornton Jones Solicitors Limited of any content, products or services which are outside our direct control.

Wills & Probate Solicitors

What Are Statutory Trusts That Arise on Intestacy?

When someone dies without a valid Will, they are said to have died intestate. In England and Wales, their estate is then distributed under the rules of intestacy, set out in legislation. In many cases, those rules create what are known as statutory trusts.

What is a Statutory Trust?

A statutory trust is a trust that arises automatically by law, rather than being deliberately created by a Will.

Under the intestacy rules, certain beneficiaries (most commonly children) do not receive their inheritance outright immediately. Instead, their entitlement is held on trust until specific conditions are met.

When Do Statutory Trusts Arise?

Statutory trusts commonly arise where the deceased is survived by:

- children, or

- other close family members who are entitled under the intestacy rules

The most common example is where a person dies leaving children under the age of 18.

Who Benefits Under a Statutory Trust?

Under the rules of intestacy, beneficiaries typically include:

- children (including legally adopted children), and

- their descendants if a child has already died

Each beneficiary is entitled to a share of the estate, but that share is held on statutory trust until they are legally entitled to receive it outright.

What are the Rules of Intestacy?

The Rules of Intestacy can be quite complex to understand, particularly if there are a significant number of beneficiaries. If you are married and have children, only the first £322,000 will pass to your surviving spouse, the remainder will be divided between your children and your spouse. Read more…

When Does a Beneficiary of a Statutory Trust Become Entitled?

Under a statutory trust, a beneficiary becomes absolutely entitled when they:

- reach 18 years of age, until then, their inheritance is held and managed by trustees.

Who Acts as Trustee of a Statutory Trust?

The personal representatives (usually the administrators of the estate) act as trustees of the statutory trust. They are responsible for:

- safeguarding the assets

- managing investments

- applying income or capital for the beneficiary’s benefit where appropriate

This role carries legal duties and responsibilities.

What Can the Trustees of a Statutory Trust Do With the Funds?

Trustees have limited statutory powers, including the ability to:

- use income or capital for a child’s maintenance, education or benefit, and

- invest the funds until the beneficiary becomes entitled

However, the flexibility is far more restricted than if a tailored trust had been created by a Will.

"*" indicates required fields

Why Can Statutory Trusts Be Problematic?

Statutory trusts are one-size-fits-all and may not reflect what the deceased would have wanted. Common issues include:

- beneficiaries inheriting outright at 18, regardless of maturity

- no scope to protect assets from divorce, creditors or poor decision-making

- no ability to benefit stepchildren or unmarried partners

- increased administrative burden for trustees

How Can You Avoid a Statutory Trust Being Invoked?

The only way to avoid statutory trusts arising on death is to have a properly drafted Will. A Will allows you to:

- choose who inherits

- decide when and how beneficiaries receive their inheritance

- appoint trustees of your choosing

- include flexible trust arrangements where appropriate

Contact our Wills & Probate Solicitors for Advice

Understanding statutory trusts highlights why estate planning is so important and why dying without a Will can leave loved ones with outcomes you never intended.

At Thornton Jones Solicitors our private client team can assist you in preparing a Will that reflects your wishes and will avoid unintended consequences. Contact our friendly and professional team today for more information.

If you need assistance or advice you can contact our team today on 01924 290 029 or contact us using our online enquiry form.

Statutory Trust FAQs

A statutory trust arises automatically under the rules of intestacy when someone dies without a valid Will. In contrast, a trust created by a Will is deliberately set up by the person who has died, allowing them to control how and when beneficiaries receive their inheritance.

Under a statutory trust, children usually become entitled to their inheritance when they reach 18. Until then, their share of the estate is held and managed by trustees on their behalf.

Statutory trusts are automatically created by law under the rules of intestacy, most commonly to manage the inheritance of minors. While you cannot remove the legal effect once the trust arises, there are ways to manage or conclude it. For example, the trust automatically ends when a beneficiary reaches 18, giving them full entitlement to their share. Trustees may also, in certain cases, convert the statutory trust into a bare trust to give the beneficiary more control over the assets.

The most effective way to avoid a statutory trust entirely is to make a valid Will. By doing so, you can specify who inherits, when they inherit, and under what conditions, ensuring your estate is distributed according to your wishes rather than default intestacy rules. Proper estate planning also reduces administrative burdens and helps protect assets from unintended risks.

The content of this blog post is for information only and does not constitute formal legal advice and should not be relied upon as advice. Thornton Jones Solicitors Limited accepts no liability for any such reliance upon this content. Where the post includes links to external websites, Thornton Jones Solicitors Limited accepts no responsibility for the content of such sites. Any link to a third-party website should not be construed as endorsement by Thornton Jones Solicitors Limited of any content, products or services which are outside our direct control.

Wills & Probate Solicitors

Who can be my Executor? Professional Executors vs. Lay Executors

When providing instructions for a Will, the Testator will be asked to name an Executor within the terms of the Will. At the very least, they will be asked to appoint one Executor and at the most they can appoint four Executors.

What is an Executor to a Will?

An Executor to a Will is someone who will be responsible upon the Testator’s death to manage the deceased’s estate. It is their duty to ensure that the following are completed:

- The deceased’s wishes are carried out;

- All assets have been identified and disposed of in accordance with the Will;

- All liabilities including debts, taxes and testamentary expenses have been settled; and

- A Grant of Probate has been obtained, if required.

The role is not restricted to the above points; however, these obligations will take up most of the Executor’s time and focus.

Who can be an Executor of a Will?

In England and Wales, anyone is eligible to be appointed as an Executor as long as they are over the age of 18 and have mental capacity to undertake and perform the duties of an Executor.

Usually, people appoint their close family members or close friends as Executors. For example, their spouse, children, parents, siblings, lifelong friends etc. These kinds of Executors are known as Lay Executors.

However, professionals can also be appointed as Executors too, i.e. solicitors. These are referred to as Professional Executors. Professional Executors can be appointed when there is no-one you feel is willing or suitable to take this role on but also for a number of other reasons too.

Can a Beneficiary of a Will also be the Executor?

An Executor can also be a beneficiary under the terms of the Will. For example, if you appoint your spouse as an Executor and everything is to pass to them upon your death, this will not prevent them from acting as an Executor.

It is entirely up to the Testator who they wish to pick to be their Executor. When considering this decision, they may contemplate what is best suited to their specific circumstances and how they wish for their estate to be dealt with upon their death. It is important to note that Executors can be changed by updating your Will and it is not a definitive decision.

What are the Rules of Intestacy?

The Rules of Intestacy can be quite complex to understand, particularly if there are a significant number of beneficiaries. If you are married and have children, only the first £322,000 will pass to your surviving spouse, the remainder will be divided between your children and your spouse. Read more…

What are the benefits of appointing a Lay Executor?

1. Trust and Personal Knowledge

When appointing a Lay Executor, this is likely to be someone close to you and who knows you on a personal level. Therefore, when dealing with the estate administration they are likely to make decisions in consideration of your personal wishes. For example, if they were planning your funeral, it is likely that they would take a personable approach by considering your wishes, such as having consideration to religious beliefs, music choices and desires regarding burial or cremation.

Another example where a personal approach may be taken is in regard to the distribution of personal items, i.e., jewellery, they may have knowledge that something is a family heirloom so you may wish for this to be passed on to a family member rather than this being discarded.

Having an Executor act who has known you and has prior knowledge of your circumstances can be a useful when dealing with the Estate. This can help the Executor navigate the administrative process with care and respect to your personal wishes. It is also advantageous when dealing with family of the deceased and handling their dynamics. They may understand certain situations need to be handled carefully and proceed to deal with sensitive situations with compassion.

Appointing a family member or friend to be an Executor may give the deceased peace of mind due to the implicit trust and faith they have in the individual to deal with matters how they would like.

2. Saving on Legal Costs

Appointing a family member or friend to be the Executor to deal with the estate administration can save on legal costs. They have no rights to charge for this service and cannot profit from undertaking the role.

It is the Executor’s discretion if they seek legal advice and instruct solicitors to help them with the administrative process. If they choose not to, the estate will not bear a burden of settling legal costs unlike if a Professional Trustee was acting.

However, Executors are entitled to claim back their expenses from the estate funds. For example, payment of death certificates, the probate application fee, administrative costs etc but they cannot charge for their time and dedication to the role.

3. Flexibility and Informality

Choosing a Lay Executor may be mean that the estate is dealt with on a more informal basis. For example, communications with beneficiaries may be more causal. Lay Executors may explain the processes in plain language and remove the legal jargon which can arise when solicitors are dealing with an estate.

In addition, a Lay Executor may have increased understanding towards the deceased’s family dynamics. They may have the potential to foresee anticipated disputes, and this can be helpful when managing the expectations of those involved, minimising tensions and resolving conflict. They are likely to understand any emotional ties to personal and sentimental items and consider who may wish to retain such items within the family.

Flexibility and informality can mean that there is more natural communication between the Executor and beneficiaries, and the Lay Executor could use their emotional awareness to manage the family’s needs and expectations by making relationship-sensitive decisions. However, the informal and flexible approach should not compromise them in their role to comply with the legal framework of the estate administration.

In summary, Lay Executors can bring a more personal approach to the estate administration and at a lower cost than a Professional Executor.

"*" indicates required fields

What are the benefits of appointing a Professional Executor?

1. Legal Expertise and Taxation Knowledge

Estate administration can involve many complex tasks, for example: –

- Completion of a probate application;

- Inheritance Tax calculations;

- Payments of Income Tax, Capital Gains Tax and Inheritance Tax;

- Property transfers and sales;

- Business and share valuations; and

- Dealing with creditors

The list is not exhaustive, however many of the tasks can be hard to navigate with no legal training or background. A legal professional will be highly skilled and has been legal trained, therefore if acting as a Professional Executor they can understand and apply their knowledge regarding estate administration and taxation laws to those specific circumstances; understand compliance and rules relating to reporting such information and the deadlines they carry, which can reduce the risks of making costly mistakes.

Due to little understanding, Lay Executors can make small errors which can be hard to fix, by simply not having the deeper knowledge to assist them in the estate administration. Professional Executors have expert knowledge, and they are trained to avoid making such mistakes.

2. Complex and High Value Estates

The higher the value of the Estate, the more technical the Estate becomes to administer. Estates which include multiple properties, assets overseas, trusts, agricultural and business assets and large investments bring their own technical complexities. Taxation reliefs become more important to consider, and Inheritance Tax liabilities are more likely to arise. These kinds of estates can be overwhelming for a Lay Executor to navigate and understand. Therefore, a Professional Executor will have more experience on how to handle high-net worth estates and can apply their knowledge to tax-planning and complex points of law.

3. Managing Family Disputes

Often people opt to appoint Professional Executors to act when there are ongoing family tensions or history of family disputes, as they can offer an impartial and unbiased approach to the estate administration.

Tensions can arise between families at any point, i.e., during the Testators lifetime or upon death and these can impact the administration of the Estate. For example, when relatives have been treated unequally in the Will, ex-partners or blended families have grievances against the terms of the Will and dependants may wish to challenge the Will. This can develop into litigious proceedings and be difficult for Lay Executors to deal with.

If this is likely to happen, a Professional Executor may be more advantageous to have appointed as they can act independent to the ongoing conflict. Professionals have no emotional involvement, and they are obligated to distribute the Estate strictly in line with the Will. Professional Executors will take an unbiased approach to such circumstances, and this can help protect the estate from litigious proceedings.

4. Protecting Family Members from Stress

Loosing someone close to you then having to act as a Lay Executor can be an emotional challenge. Dealing with grief and a loved one’s Estate can cause great stress and anxiety.

The process of dealing with estate administration is burdensome on a Lay Executor, as it is time-consuming, administrative and often overwhelming. It can involve a volume of paperwork, handling distressed beneficiaries, managing property sales and sorting through personal belongings which can be hard when navigating grief.

Appointing a Professional Executor can remove the emotional ties and protect family members from the extra burden of dealing with a loved one’s Estate. They will have the time to grieve without the administrative pressure and the freedom to process their emotions without having to deal with lengthy legal matters.

5. Continuity and Reliability

Appointing a Professional Executor can ensure some structure and consistency when dealing with the estate administration. As they are acting in their professional capacity, they must remain impartial and unbiased in order to uphold their profession’s code of conduct, meaning that can be trusted and deal with the Estate in an ethical and efficient manner.

They also have internal systems and procedures, meaning that every decision or step taken in relation to progressing the matter will be documented and recorded to ensure a smooth and fluid transition through the administrative process. Internal procedures ensures that work can be delegated to other members of the team so work can be actioned in a timely and smooth manner.

It is unlikely that a solicitor will die or become incapacitated during the administration period, unlike the appointment of an elderly relative such as a sibling or parent. If a solicitor does become unable to act, it will become less problematic than if this were to happen to a Lay Executor. Another member of the Firm would likely step in to replace the Professional Executor.

Having a Professional Executor making decisions in regard to the Estate can ensure that it is dealt with in an efficient and reliable manner.

6. Reduce Personal Liability Risk

Executors can become personally liable if they distribute assets before settling debts, miscalculate tax owed from the estate, fail to identify claims against the estate or breach fiduciary duties. This means that they can find themselves in a position whereby they are owing monies to creditors and beneficiaries from their personal finances, through innocent and small errors.

Appointing a Professional Executor would ensure that a Lay Executor does not become liable in these circumstances. Professional Executors have a thorough understanding of mitigating risks and following formal procedures. They understand how to protect themselves in this instance by keeping detailed accounts and contacting and notifying creditors to ensure all debts are settled. They have access to conducting financial searches to identify any liabilities and are able to publish specialised notices to creditors. This protects family members and friends from compromising themselves financially through minor and naïve errors.

Overall, Professional Executors can take an unbiased approach and take on the majority of the administrative and time-burdensome work. They can apply their legal expertise to decisions made in relation to the Estate in order to mitigate risks and errors which can cause personal liability to arise.

Conclusion

In conclusion, there is no right or wrong answer as to who an Executor can be. Both Lay Executors and Professional Executors have their own advantages but there is not a one size fits all answer.

When choosing an Executor to appoint, it is advisable to consider the bigger picture and your personal circumstances, by making a balanced and informed choice what you as a Testator will be comfortable with upon death.

How can Thornton Jones help?

Here at Thornton Jones, we can offer bespoke advice regarding the role of Executors. We can assist you in deciding who to choose to be an Executor in your Will by providing you with detailed information relating to the appointment of Lay Executors and Professional Executors and updating your Will in this regard.

In most circumstances, the Directors of Thorntons Jones are willing to be appointed as Professional Executors and we can explain how this would work in terms of your Estate, such as how we can offer a personal element, who would handle the estate day to day and any fees which this may incur.

Our experienced team can also assist any Lay Executors who may be struggling with the estate administration and need some extra support and advice in this regard. If appropriate, they assist with more limited work such as applying for probate or offering bespoke and specific advice in relation to your role as a Lay Executor. They can also assist with dealing with high value and complex estates and can take on the full estate administration and reduce the burden of this upon the individual where appropriate.

Contact our Wills & Probate Solicitors for Advice

Choosing the right Executors and preparing a clear Will are key steps to ensure your estate is managed according to your wishes. Without a Will, statutory trusts may determine who inherits, potentially creating outcomes you did not intend and leaving loved ones in a difficult position.

At Thornton Jones Solicitors, our Private Client team can guide you through appointing Executors you trust and drafting a Will that reflects your intentions. We help you plan ahead so your estate is handled smoothly and in line with your wishes.

For personalised advice or assistance, contact our team today on 01924 290 029 or via our online enquiry form. We’re here to help you make the right choices for your estate and your loved ones.

Executor of a Will FAQs

The key distinction lies in their roles within the context of a Will. The testator is the individual who creates the Will, setting out their wishes regarding how their estate should be managed and distributed after their death. As part of this process, the testator may specify that certain assets, or a portion of their estate, are to be placed into a trust for the benefit of particular individuals.

The executor, on the other hand, is the person appointed in the Will to carry out those wishes. Their responsibilities include collecting and valuing the estate, settling any outstanding debts, taxes, and administrative expenses, and ensuring that any specific gifts are distributed correctly and in accordance with the wishes of the Testator.

You can appoint up to four executors to your Will in the UK, although only one is strictly required. It is common and recommended to appoint at least two Executors to share the workload, provide backup if one is unable to act, and ensure security. All appointed executors must act jointly.

A lay executor (usually family/friends) acts unpaid, offering a personal, cost-effective service, whereas a professional executor (e.g., solicitor) charges fees for expert, impartial, and insured estate administration. Lay executors are suitable for simple estates, while professionals reduce risk in complex scenarios involving tax, trusts, or potential disputes.

The content of this blog post is for information only and does not constitute formal legal advice and should not be relied upon as advice. Thornton Jones Solicitors Limited accepts no liability for any such reliance upon this content. Where the post includes links to external websites, Thornton Jones Solicitors Limited accepts no responsibility for the content of such sites. Any link to a third-party website should not be construed as endorsement by Thornton Jones Solicitors Limited of any content, products or services which are outside our direct control.

Contact our Wills & Probate Solicitors in Garforth, Leeds

Thornton Jones Solicitors

Westbourne House

99 Lidgett Lane

Garforth

Leeds

LS25 1LJ

Tel: 0113 246 4423

Fax: 0113 831 4929

Email: enquiries@thorntonjones.co.uk

Contact our Wills & Probate Solicitors in Wakefield

Thornton Jones Solicitors

Bank House

1 Burton Street

Wakefield

WF1 2GF

Tel: 01924 290029

Fax: 01924 290240

Email: enquiries@thorntonjones.co.uk

Contact our Wills & Probate Solicitors in Ossett, Wakefield

Thornton Jones Solicitors

25 Bank Street

Ossett

WF5 8PS

Tel: 01924 586466

Fax: 01924 290240

Email: enquiries@thorntonjones.co.uk

Contact our Wills & Probate Solicitors in Sherburn in Elmet, Leeds

Thornton Jones Solicitors

6 Finkle Hill

Sherburn in Elmet

Leeds

LS25 6EA

Tel: 01977 350500

Fax: 0113 831 4929

Email: enquiries@thorntonjones.co.uk

Fast, Free and Risky: Why You Shouldn’t Use AI to Write Your Will

Artificial intelligence is becoming part of everyday life. From drafting emails to answering questions and generating documents, it can feel quick, convenient and cost-effective. It’s therefore no surprise that some people are considering using AI tools to prepare their Will.

Is It Safe to Use AI to Write My Will?

Whilst AI can be a helpful starting point for understanding many legal concepts, it is far from a suitable substitute for expert and tailored legal advice from a trained legal professional, particularly when it comes to something as important as drafting your Will.

A Will Is Not a Standard Document

No two clients are the same. All individuals have different family structures and dynamics, different assets, business interests, tax positions and personal wishes and all of these things impact how a Will should be drafted.

AI works by producing generic wording based on common patterns and probabilities. It cannot properly assess:

- blended families or second marriages

- vulnerable beneficiaries

- overseas assets

- business or agricultural property

- trusts, life interests or discretionary arrangements

A Will that looks fine on the surface may indeed be legally valid but wholly inappropriate for your specific personal circumstances which can lead to significant problems in the future.

AI Cannot Give Legal Advice or Spot Risks in Your Wishes

A solicitor’s role is not just to write down what you say, it is to listen, to ask the right questions, to flag potential problems with your wishes and to explain the consequences of the different choices you wish to make.

When making a Will AI cannot:

- advise on inheritance tax planning

- assess capacity or undue influence

- warn you about potential claims under the Inheritance (Provision for Family and Dependants) Act 1975

- ensure your wishes are clear enough to avoid disputes

These are often the very issues that lead to costly disputes and litigation after death.

"*" indicates required fields

Errors in your Will May Only Come to Light When It Is Too Late

One of the greatest risks with AI-generated Wills is that mistakes are often only discovered after death, when they cannot be corrected.

Common problems include:

- unclear or contradictory clauses

- gifts failing due to the incorrect wording being used

- executors lacking the necessary powers they require to assist in the administration

- invalid execution or witnessing of the Will

At that point, the cost of fixing the problem usually far exceeds the cost of having the Will professionally prepared by a Solicitor in the first place.

Capacity, Safeguarding and Record-Keeping Matter

Solicitors are trained to assess testamentary capacity and to identify red flags around vulnerability or pressure from others. We also keep detailed attendance notes and records that can be crucial if a Will is later challenged.

AI tools cannot:

- assess testamentary capacity

- protect against coercion

- provide evidence if the Will is disputed

These safeguards are a vital part of proper Will-making.

Do I need to register my Trust with HMRC?

Most trusts in the UK must be registered with HMRC’s Trust Registration Service, but certain trusts are exempt, such as those imposed by a court or created through legislation. Trustees are legally responsible for ensuring registration where required. Failing to do so can lead to penalties, so it is important to confirm your obligations with a solicitor or a tax adviser. Read more…

Convenience Should Not Outweigh Certainty

AI can be fast, but speed should not be the priority when dealing with your estate and your family and loved one’s future.

Using AI may feel efficient now, but it carries significant legal and financial risk later.

Contact our Wills and Probate Solicitors for Advice

At Thornton Jones Solicitors we use the appropriate technology in places where it enhances efficiency, but be assured that your Will is always prepared by an experienced solicitor who understands the law and, crucially, your individual circumstances.

At Thornton Jones our Private Client Solicitors will:

- take time to understand your wishes and you unique family situation

- advise on inheritance tax, trusts and future planning

- ensure your Will is clear, valid and robust

- provide advice to reduce the risk of disputes after death

Your Will is one of the most important documents you will ever sign. It deserves more than a generic template, it deserves proper legal advice.

Our experienced Wills and Probate team will are here to advise you when making your Will to ensure that the final document accurately reflects your wishes.

If you need assistance or advice you can contact our team today on 01924 290 029 or contact us using our online enquiry form.

Wills and Probate Solicitors FAQs

Testamentary capacity refers to a person’s legal ability to make or change a valid Will. Under English law, the person making the Will (known as the testator) must understand that they are making a Will, understand the nature and extent of their assets, and recognise who might reasonably expect to benefit from their estate. Wills can be challenged on the basis of a testator lacking testamentary capacity at the time the Will was prepared. A testator may lack testamentary capacity due to reasons of illness, cognitive impairment or vulnerability.

Coercion when making a Will occurs when someone may pressure, threaten or manipulate the person making the Will into including provisions they would not otherwise choose that may benefit them or another person. This pressure can take many forms, emotional, psychological or even physical. This type of behaviour is sometimes referred to as undue influence. If a court finds that the Will was made under undue influence, it can be declared invalid, because it does not reflect the true wishes of the testator.

The Inheritance (Provision for Family and Dependants) Act 1975 allows certain individuals to make a legal claim against a deceased person’s estate if they believe they have not been left reasonable financial provision. Eligible claimants may include spouses, civil partners, children, cohabiting partners, or dependants of the deceased. The court can redistribute part of the estate if it considers the Will or intestacy rules do not provide adequate financial support.

The content of this blog post is for information only and does not constitute formal legal advice and should not be relied upon as advice. Thornton Jones Solicitors Limited accepts no liability for any such reliance upon this content. Where the post includes links to external websites, Thornton Jones Solicitors Limited accepts no responsibility for the content of such sites. Any link to a third-party website should not be construed as endorsement by Thornton Jones Solicitors Limited of any content, products or services which are outside our direct control.

Contact our Wills and Probate Solicitors in Garforth, Leeds

Thornton Jones Solicitors

Westbourne House

99 Lidgett Lane

Garforth

Leeds

LS25 1LJ

Tel: 0113 246 4423

Fax: 0113 831 4929

Email: enquiries@thorntonjones.co.uk

Contact our Wills and Probate Solicitors in Wakefield

Thornton Jones Solicitors

Bank House

1 Burton Street

Wakefield

WF1 2GF

Tel: 01924 290029

Fax: 01924 290240

Email: enquiries@thorntonjones.co.uk

Contact our Wills and Probate Solicitors in Ossett, Wakefield

Thornton Jones Solicitors

25 Bank Street

Ossett

WF5 8PS

Tel: 01924 586466

Fax: 01924 290240

Email: enquiries@thorntonjones.co.uk

Contact our Wills and Probate Solicitors in Sherburn in Elmet, Leeds

Thornton Jones Solicitors

6 Finkle Hill

Sherburn in Elmet

Leeds

LS25 6EA

Tel: 01977 350500

Fax: 0113 831 4929

Email: enquiries@thorntonjones.co.uk

It’s Update Your Will Week 2026

This Update Your Will Week – 2nd to 8th March 2026, we are proud to support The Association of Lifetime Lawyers in raising awareness about the importance of both making a Will, as well as keeping your Will up to date if personal circumstances change.

Is your Will still right for you?

A Will is far more than just legal document. It captures your wishes, protects your loved ones, and safeguards the legacy you want to leave behind. Modern families are changing rapidly, and people often wrongly assume that their loved ones will be automatically taken care of. However, without clear and legally valid instructions, families and partners can face uncertainty, distress, and even costly disputes-often discovering too late that assumptions do not provide protection under the law and can have serious consequences

Why updating your Will matters

Your Will ensures that your money, property, and personal possessions pass to the people you choose. If you have children under the age of 18, you can also appoint legal guardians in your Will. And if you have pets, you can decide who will look after them after your passing. But when did you last review yours? If your Will is not up to date or you don’t have a Will:

- your estate may be distributed under the intestacy rules, which might not reflect your wishes or your family’s needs.

- loved ones could face unnecessary stress, delays, or legal disagreements at an already difficult time. Your Will should be treated as a living document-evolving as your circumstances change. Regular reviews aren’t a luxury; they’re an essential part of protecting the people you care about.

"*" indicates required fields

When should you update your Will?

It’s best practice to review your Will every three to five years or after any major life event, such as:

- Getting married or entering a civil partnership

- Getting divorced or dissolving a civil partnership

- Becoming a parent or grandparent

- Buying a home or changing your financial situation

- Losing a loved one

- Starting a business

- You or a beneficiary obtaining a Gender Recognition Certificate

What Are The Risks of Using Unregulated Will Writers in the UK?

Making a Will is a vital step in ensuring that your assets are passed on according to your wishes and that your loved ones are taken care of after you’re gone. However, an increasing number of people are turning to unregulated Will writers, often drawn in by low fees, promises of simplicity, and sometimes even the offer of a free gift! A blog by Stacie Hurt.

Need to make or update your Will?

If it’s been a while since you last looked at your Will, or you don’t have one yet, now is the time to take action. At Thornton Jones Solicitors our Private Client team offer specialist expertise in later-life legal matters.

We can help families put clear, legally robust arrangements in place that reflect real lives. We aim to provide personalised support with care, empathy, and attention to detail, ensuring your wishes are clearly documented and legally protected.

Don’t wait until it’s too late, ensure your future wishes are in place today. If you need to make or update your Will, contact our team on 01924 290 029 or contact us using our online enquiry form for expert advice today.

Update Your Will Solicitors FAQs

It’s sensible to review your will every three to five years, or sooner if you experience a major life event such as marriage, divorce, the birth of a child, buying property, or a significant change in financial circumstances. Regular reviews ensure your wishes remain accurate and legally effective.

Failing to update your will can lead to unintended consequences. For example, marriage can revoke an existing will (unless made in contemplation of marriage), and divorce may affect how gifts to a former spouse are treated. An outdated will can create uncertainty, delay administration of your estate, and increase the risk of disputes.

Minor amendments can be made using a codicil, but significant changes are often best dealt with by preparing a new will. Attempting to alter a will yourself, for example, by crossing out sections, can invalidate it or cause confusion. Seeking legal advice ensures your updated will is properly drafted and executed in line with English law.

The content of this blog post is for information only and does not constitute formal legal advice and should not be relied upon as advice. Thornton Jones Solicitors Limited accepts no liability for any such reliance upon this content. Where the post includes links to external websites, Thornton Jones Solicitors Limited accepts no responsibility for the content of such sites. Any link to a third-party website should not be construed as endorsement by Thornton Jones Solicitors Limited of any content, products or services which are outside our direct control.

Contact our Wills and Probate Solicitors in Garforth, Leeds

Thornton Jones Solicitors

Westbourne House

99 Lidgett Lane

Garforth

Leeds

LS25 1LJ

Tel: 0113 246 4423

Fax: 0113 831 4929

Email: enquiries@thorntonjones.co.uk

Contact our Wills and Probate Solicitors in Wakefield

Thornton Jones Solicitors

Bank House

1 Burton Street

Wakefield

WF1 2GF

Tel: 01924 290029

Fax: 01924 290240

Email: enquiries@thorntonjones.co.uk

Contact our Wills and Probate Solicitors in Ossett, Wakefield

Thornton Jones Solicitors

25 Bank Street

Ossett

WF5 8PS

Tel: 01924 586466

Fax: 01924 290240

Email: enquiries@thorntonjones.co.uk

Contact our Wills and Probate Solicitors in Sherburn in Elmet, Leeds

Thornton Jones Solicitors

6 Finkle Hill

Sherburn in Elmet

Leeds

LS25 6EA

Tel: 01977 350500

Fax: 0113 831 4929

Email: enquiries@thorntonjones.co.uk

What is a Discretionary Trust?

When people are planning for their future, most have two objectives, to protect their assets and provide for their loved ones. A Discretionary Trust is a legal structure that can offer both. It allows you to safeguard your wealth, maintain some control, and ensure your beneficiaries are looked after. It also provides the flexibility to deal with changing circumstances over the passage of time and a number of different scenarios that may arise.

What Is a Discretionary Trust?

A Discretionary Trust is a Trust Deed that can be created during your lifetime, or upon your death by the terms of your Will. The structure of a Discretionary Trust enables you, as the person putting your assets or money into the trust (known as the Settlor), to give those assets to a group of people chosen by you (the Trustees) to look after for the people you want to benefit from the trust (the Beneficiaries).

As the Settlor, you may appoint yourself as a Trustee. If you would like to keep control of how the assets in the Trust are used, then you would be able to do so by being a Trustee. Whilst extracting the asset from your estate and allowing your beneficiaries to enjoy it, jointly with the other Trustees you still retain decision making power until transferred to the beneficiaries absolutely.

The Trust Deed will name the group of people who you want to benefit from those assets (the Beneficiaries). It will be at the discretion of the Trustees to decide which of the Beneficiaries to pass assets on to, when, and how much they will receive. The Trustees have the authority to decide how income and capital from the trust should be distributed among the beneficiaries.

You can leave detailed instructions and directions to the Trustees as to how you would like them to exercise their discretion by preparing a Letter of Wishes to accompany the Trust Deed. Although the Letter of wishes is not legally binding on the Trustees, they will often take them into consideration and follow your wishes as closely as possible, whilst considering other factors. This flexibility allows the Trustees to respond to changing family, financial, or tax circumstances.

Who Is Involved in a Discretionary Trust?

- Settlor: The individual who sets up the trust and transfers assets into it.

- Trustees: The people appointed to manage the trust assets in line with the trust deed.

- Beneficiaries: The individuals or groups who may benefit from the trust.

What are the advantages of a Discretionary Trust?

Asset Protection

Because of its discretionary nature, with the decision as to who benefits, when and by how much resting with the Trustees, none of the Beneficiaries are “entitled” to any of the trust fund. Therefore, assets held in a Discretionary Trust are generally protected from claims in situations like divorce, bankruptcy, or litigation. If a beneficiary is going through a divorce, an appropriate Discretionary Trust can ensure that assets from your estate won’t pass to their former spouse. Similarly, if a beneficiary is bankrupt, or in danger of becoming bankrupt, there is a real risk that with no Discretionary Trust in place, any gift from your estate could be paid directly to the Beneficiary’s creditors.

Since beneficiaries have no fixed entitlement, their creditors usually cannot access trust assets.

Estate Planning Flexibility

A Discretionary Trust helps you control how family wealth is used and distributed, even across generations. This can included business interests and family companies. It can provide for children or dependants who are not yet financially mature or have special care needs. It can provide for specific scenarios arising and changing circumstances.

If a beneficiary has a disability or is vulnerable in some way, or receives other state benefits, any money paid directly from your estate could reduce their entitlement to state support or render them ineligible completely. A trust for a vulnerable person can benefit from favourable tax treatment.

Potential Tax Planning Benefits

When used appropriately, Discretionary Trusts can offer income tax saving opportunities or structure estate transfers efficiently. However, tax treatment varies, so professional tax advice is essential.

Scope and Continuity

A Discretionary Trust can be set up during your lifetime and continue to run smoothly after your death, ensuring uninterrupted management of family wealth.

Do I need to register my Trust with HMRC?

Most trusts in the UK must be registered with HMRC’s Trust Registration Service, but certain trusts are exempt, such as those imposed by a court or created through legislation. Trustees are legally responsible for ensuring registration where required. Failing to do so can lead to penalties, so it is important to confirm your obligations with a solicitor or a tax adviser. Read more…

Tax Opportunities and Obligations of a Discretionary Trust

Income Tax

Trustees are responsible for paying Income Tax on income received by the Trust. The Trust will pay the higher rate of Income Tax. Any gross income above £500 (being the allowance for Trusts) is taxable at the current trust tax rate of 45%. Dividend income is charged at a rate of 39.35%. If the Settlor has more than one Discretionary Trust, the £500 tax free limit is divided by the number of trusts.

When Trustees pay income to a beneficiary who is taxed at less than 45% the beneficiary can reclaim the tax so that the eventual tax burden does not exceed what it would have been if the trust assets were their own.

Discretionary Trusts can be a useful tool for income tax planning, depending on the circumstances of the beneficiary.

Capital Gains Tax

This is a tax on the profit (gain) when an asset that has increased in value is taken out of or put into the Trust.

If assets are put into the Trust, the tax is paid by the person selling or transferring the asset.

If assets are taken out of the trust the Trustees usually have to pay the tax is they sell or transfer assets on behalf of the beneficiaries.

The rate of Capital Gains Tax is payable at 24% if the trust’s annual total taxable gain is greater than its tax-free allowance (£1,500 or £3,000 if the beneficiary is vulnerable. If there is more than one beneficiary, the higher allowance may apply even if only one of them is vulnerable.

Inheritance Tax

Inheritance Tax may be payable on a person’s estate when they die. Inheritance Tax can also apply when you are alive if you transfer some of your estate such as property, money, investments etc into a trust.

The main situations when Inheritance Tax is due are:

- When assets are transferred into a trust, if the value of the assets put into the trust by the settlor exceeds the £325,000 nil rate band. Where the asset qualifies for relief such as Business Property Relief then it may be that no IHT arises on the initial transfer.

- When a trust reaches it’s 10-year anniversary of being set up (10-yearly Inheritance Tax payments). This is currently up to 6%, payable on the amount by which the value of the trust fund exceeds the available nil rate band.

- When assets are transferred out of a trust, known as exit charges. This is when capital or assets are distributed from the trust to a beneficiary. These are generally a proportion of the 6% charge, depending on the time passed since the last 10-year charge.

- When somebody dies and a trust is involved.

"*" indicates required fields

What are the Duties of Trustees in a Discretionary Trust?

Trustees of Trusts should be aware of the need to comply with the HM Revenue & Customs Trust Registration Service. This is a central register that HMRC maintains of most trust arrangements, particularly express trusts (i.e. those created intentionally by the settlor). Registration is often required even if the trust has no tax to pay at the time it is created.

Trustees also have administrative obligations and duties such as keeping accounts, filing Trust Tax Returns, and ensuring the payment of tax where applicable.

Conclusion

There are a range of situations where a Discretionary Trust could provide a flexible solution for protecting your estate and your family’s future. You do not have to be wealthy to find that a Discretionary Trust can offer a flexible, effective way of passing assets onto your chosen beneficiaries.

It is important to consider who you would appoint as Trustees. They should be trustworthy, impartial where possible and financially competent.

It is important to ensure clarity as to the terms of the Trust including its powers, intent and scope.

It important to recognise and understand compliance obligations and the tax treatment associated with Discretionary Trusts, and to consider whether other planning options would be more tax effective or appropriate for your individual situation.

The key issues is to recognise that bespoke advice is needed and to seek both expert legal and financial advice as early as possible.

Contact our Discretionary Trusts Solicitors for Advice

Here at Thornton Jones, we can provide bespoke advice tailored to your circumstances.

Our experienced team will advise you on whether a Discretionary Trust suits your circumstances, or perhaps another kind of Trust, and if appropriate draft a bespoke Trust Deed to reflect your intentions, assist Trustees with administration and compliance and coordinate with financial and tax advisors where appropriate.

If you need assistance or advice you can contact our team today on 01924 290 029 or contact us using our online enquiry form.

Discretionary Trust Solicitors FAQs

Capital Gains Tax (CGT) is a tax on the profit you make when you sell or dispose of an asset that has increased in value, such as property, shares, or other investments. It is only charged on the gain, not the total sale amount, and certain exemptions, like your annual CGT allowance, may apply.

Inheritance Tax (IHT) is a tax on the estate (property, money, and possessions) of someone who has passed away. In England, it is typically charged on estates valued above a certain threshold, with exemptions available for gifts, charities, and transfers between spouses or civil partners.

Income Tax is a tax on money you earn, including wages, pensions, self-employed profits, and some savings or investment income. The rate you pay depends on your total income and the applicable tax bands, with personal allowances and reliefs reducing the amount you owe.

The content of this blog post is for information only and does not constitute formal legal advice and should not be relied upon as advice. Thornton Jones Solicitors Limited accepts no liability for any such reliance upon this content. Where the post includes links to external websites, Thornton Jones Solicitors Limited accepts no responsibility for the content of such sites. Any link to a third-party website should not be construed as endorsement by Thornton Jones Solicitors Limited of any content, products or services which are outside our direct control.

Contact our Discretionary Trust Solicitors in Garforth, Leeds

Thornton Jones Solicitors

Westbourne House

99 Lidgett Lane

Garforth

Leeds

LS25 1LJ

Tel: 0113 246 4423

Fax: 0113 831 4929

Email: enquiries@thorntonjones.co.uk

Contact our Discretionary Trust Solicitors in Wakefield

Thornton Jones Solicitors

Bank House

1 Burton Street

Wakefield

WF1 2GF

Tel: 01924 290029

Fax: 01924 290240

Email: enquiries@thorntonjones.co.uk

Contact our Discretionary Trust Solicitors in Ossett, Wakefield

Thornton Jones Solicitors

25 Bank Street

Ossett

WF5 8PS

Tel: 01924 586466

Fax: 01924 290240

Email: enquiries@thorntonjones.co.uk

Contact our Discretionary Trust Solicitors in Sherburn in Elmet, Leeds

Thornton Jones Solicitors

6 Finkle Hill

Sherburn in Elmet

Leeds

LS25 6EA

Tel: 01977 350500

Fax: 0113 831 4929

Email: enquiries@thorntonjones.co.uk

Lasting Powers of Attorney: Protection You Hope You’ll Never Need

Most of us are happy to take out insurance. We insure our homes, our cars, even our holidays. Why? Because if something goes wrong, we want to know we’re protected. A Lasting Power of Attorney (LPA) works in the same way. You may never need it, but if you do, it can make all the difference to you and your loved ones.

You must remember that you can only make an LPA while you still have mental capacity. If illness, accident, or age takes that away, it’s too late. Just like with insurance, you don’t wait until the disaster has happened before putting cover in place.

What is a Lasting Powers of Attorney?

A lasting Powers of Attorney (often abbreviated to an LPA) is a legal document that lets you choose one or more people you trust to make decisions for you if, one day, you can’t make them yourself. There are two types and you should think of them as two separate insurance policies: one for your finances, one for your wellbeing. Together, they give you complete protection.

Property and Financial Affairs LPA

A Property and Financial Affairs LPA covers money matters like paying bills, managing bank accounts, pensions, and even selling your home if necessary.

Health and Welfare LPA

A Health and Welfare LPA covers personal matters like where you live, your daily care, and medical treatment, including life-sustaining treatment.

5 Benefits of a Lasting Power of Attorney

Whilst a Will can protect your family after you have passed, what about protecting yourself and your family should you find yourself unable to care for your own matters? In this blog by Liz Fyfe, she outlines five key benefits of having a lasting Powers of Attorney in place. Read more…

Why do Lasting Powers of Attorney Matter?

Without an LPA in place, your family doesn’t automatically have the right to step in and help if you lose capacity. Instead, they may need to apply to the Court of Protection – a process that can be long, stressful, and expensive.

By setting up LPAs in advance, you:

- Choose who makes decisions for you, rather than leaving it to the courts.

- Save your family unnecessary stress and costs.