The 10 Most Asked Questions in a Conveyancing Transaction Answered

At Thornton Jones Solicitors, we understand that buying or selling a property is often one of the largest financial decisions you will ever make. Whether you are moving home, purchasing your first property, or selling as part of a wider investment plan, the process can raise a lot of questions, and sometimes, a lot of worries.

Our dedicated conveyancing team has helped thousands of clients across Yorkshire and beyond navigate the legal process with confidence. We pride ourselves on being approachable, proactive and responsive, guiding you through every step with clear communication and practical advice. No unnecessary jargon. No hidden surprises. Just straightforward support when you need it most.

To help demystify the journey, we’ve pulled together the 10 questions we’re asked most frequently by both sellers and buyers. Whether you’re preparing to list your home or getting ready to make an offer, this guide will give you a clearer sense of what to expect throughout your conveyancing transaction.

Top 10 Conveyancing Questions That Sellers Ask the Most

1. How long will the sale of my property take?

Most sales take around 10–12 weeks from offer to completion, though this can vary depending on the length of the chain, mortgage arrangements, search timings and how quickly information is provided.

You can read more about timescales in this recent Blog by Zanna Bain-Calladine.

2. What documents will I need to provide when I sell my home?

Your solicitor will guide you through a series of property forms, including the TA6 (Property Information Form), TA10 (Fixtures & Fittings) and, if leasehold, the TA7. You’ll also need to provide ID and details of any works carried out on the property.

You can find out more about why you must provide ID in this Blog by Alison Jewell.

3. When selling my property, when should I instruct a solicitor?

We recommend instructing us as soon as you have accepted an offer. This allows us to gather the necessary information and provide you with a quote accordingly.

4. What happens with my mortgage on completion?

Your mortgage doesn’t need to be cleared in advance. We will receive a redemption figure from your lender and repay the mortgage directly from the sale proceeds.

5. What does “exchange of contracts” mean when selling my home?

Exchange is the point the transaction becomes legally binding. After exchange, both parties commit to the sale and agree a fixed completion date.

You can find out more about exchange of contracts in this Blog by Claire Smith.

6. When selling my home do I need to move out on completion day?

Yes. Completion transfers ownership to the buyer, and you will need to vacate the property by the agreed time.

7. When I sell my home what happens with any fixtures and fittings?

The TA10 form sets out which items will remain. Completing this accurately helps avoid disputes and ensures the buyer knows exactly what is included.

8. When selling a property what is a management pack (for leasehold sales)?

Leasehold transactions require an LPE1/management pack. This is provided by the freeholder or managing agent and contains essential financial and legal information. Ordering this early is important, as it can take time to obtain.

9. How are estate agent fees paid once I have sold my property?

Your solicitor pays these from the sale proceeds on completion in accordance with your agreement with the agent.

10. When selling my home what if the buyer pulls out?

Up until exchange, either party may withdraw without penalty. After exchange, financial consequences apply if either party fails to complete.

Why Do Conveyancers Require Proof of Source of Funds?

When purchasing a property, your conveyancer will request proof of the source of your funds. While this may initially seem unnecessary, it is in fact a legal requirement and an essential safeguard in the conveyancing process. Establishing the legitimacy of monies used in a property purchase protects clients, conveyancers, and the wider property market.

Top 10 Conveyancing Questions That Buyers Ask the Most

1. How long does buying a home take?

Purchases typically take 10–12 weeks, though chains, surveys, mortgage delays and local search turnaround times can affect this.

You can read more about timescales in this recent Blog by Zanna Bain-Calladine.

2. If I want to buy a home when should I apply for a mortgage?

A mortgage agreement in principle is helpful before making an offer. Once your offer is accepted, your full mortgage application should be submitted promptly.

3. When buying a property what are “searches” and why do I need them?

Searches uncover important information about the property and surrounding area, things you wouldn’t see during a viewing. These include local authority, drainage, water, mining and environmental searches.

4. Do I need a survey when I purchase a property?

While not legally required, a survey is highly recommended. It can reveal structural issues or defects that may affect your decision or the price you’re willing to pay.

5. What’s the difference between exchange of contracts and completion?

- Exchange: The contract becomes legally binding to complete on a certain day.

- Completion: The property legally becomes yours and you can collect the keys.

6. How much deposit is paid at exchange of contracts?

Typically 10% of the purchase price is payable at exchange, although this can vary depending on your circumstances.

7. When do I pay Stamp Duty on a property purchase?

Your Stamp Duty Land Tax (SDLT) must be paid shortly after completion. We will calculate the amount due and submit the return for you.

Find out more about Stamp Duty and the recently Stamp Duty land Tax changes in this Blog.

8. What checks will my solicitor carry out when I buy a property?

We will review the title, searches, leasehold documents (if applicable), raise enquiries, and ensure your mortgage offer matches the property details.

9. When buying a property, how does the money move on completion day?

We will arrange for your deposit and mortgage funds to be in place. On the day, we transfer the purchase price to the seller’s solicitor, and once received, the keys are released.

10. When I buy a property when do I officially become the owner?

After completion, we register your ownership with the Land Registry. Once processed, you will receive confirmation of registration.

How Thornton Jones Solicitors Can Support You

Whether you are buying or selling a property, having the right legal support can make all the difference. Our experienced conveyancing team is here to:

- Provide clear, jargon-free advice at every stage of your transaction

- Keep your matter progressing efficiently with proactive communication

- Identify and resolve potential issues early to avoid unnecessary delays

- Guide you through key milestones, from instruction to completion

We understand that every transaction is unique, and we are committed to making the process as smooth and stress-free as possible.

If you are preparing to buy or sell, or simply need guidance on the next steps, our team is here to help.

For advice, assistance or to instruct us for your property sale or purchase please contact our team today on 01924 290 029 or via our online enquiry form.

The content of this blog post is for information only and does not constitute formal legal advice and should not be relied upon as advice. Thornton Jones Solicitors Limited accepts no liability for any such reliance upon this content. Where the post includes links to external websites, Thornton Jones Solicitors Limited accepts no responsibility for the content of such sites. Any link to a third-party website should not be construed as endorsement by Thornton Jones Solicitors Limited of any content, products or services which are outside our direct control.

Residential Conveyancing Solicitors

Understanding the Current HM Land Registry Registration Delays

At Thornton Jones Solicitors, we know that delays at HM Land Registry (HMLR) have become one of the most common concerns raised by clients after completion. What once took a matter of weeks can now take many months, and in more complex cases, more than a year. These delays are affecting property owners, buyers, sellers, developers, lenders and conveyancers alike.

HM Land Registry currently receives millions of applications each month, and although many simple updates are processed quickly, the growing volume of complex registrations has placed significant pressure on the system. The organisation has stated that it is actively working to improve overall turnaround times through increased staffing, investment in digital systems, and enhanced processes to reduce errors and administrative hold‑ups. Despite these efforts, backlogs remain, and it is important for property owners to understand what this means for their transaction and how they can protect themselves throughout the process.

Why Are Land Registry Delays Happening?

There are a number of key factors that are contributing to prolonged registration timelines.

High Application Volumes

HM Land Registry receives approximately 2.2 million applications each month, creating a heavy workload and inevitable bottlenecks where manual caseworker involvement is required.

Complexity of Modern Applications

While simple register updates can be processed within minutes, more detailed changes such as transfers of part, new leases, new build registrations and first registrations can take many months, often stretching from 10 to 14 months depending on the complexity.

Digital Transformation & Quality Checks

HM Land Registry’s move toward improved digital systems has introduced new quality checks designed to reduce errors. These checks can trigger requisitions when further information is needed. While intended to improve accuracy long‑term, they contribute to short‑term delays.

Post‑Pandemic Backlogs

Although progress has been made, HM Land Registry acknowledges that processing times are still not where they want them to be. They continue to recruit, modernise systems and streamline workflows to reduce the existing backlog.

Current Processing Times at HM Land Registry

The most recent published figures (updated early 2026) show the following typical timelines:

Simple Changes (e.g., removing a mortgage, name change)

- Work begins within 5 months

- Typically completed within 5–6 months, unless further information is required

More Detailed Changes (e.g., transfer of ownership, rights of way)

- Work begins within 10 months

- Usually completed within 10–12 months, but can extend to 18 months

First Registrations

- Work begins within 9 months

- Generally completed within 10–12 months, sometimes up to 18 months

New Builds, New Leases & Transfers of Part

- Work begins within 10 months

- Often completed within 11–13 months, and more complex cases may take 23–25 months

Am I Protected During the Delays at HM Land Registry?

Yes. HM Land Registry confirms that your legal rights are protected from the moment they receive your application, not when they finish processing it. This means that even if registration takes many months, ownership and lender interests remain secure.

Why Do Conveyancers Require Proof of Source of Funds?

When purchasing a property, your conveyancer will request proof of the source of your funds. While this may initially seem unnecessary, it is in fact a legal requirement and an essential safeguard in the conveyancing process. Establishing the legitimacy of monies used in a property purchase protects clients, conveyancers, and the wider property market.

What is HMLR Doing to Improve Processing Times?

HMLR has taken several steps to address delays:

Expanded Recruitment & Training

Thousands of new staff have been recruited and trained to increase capacity.

Enhanced Digital Checks

New digital systems aim to prevent simple errors at submission, reducing the number of requisitions and improving overall speed.

Greater Transparency

HMLR is now publishing data on avoidable requisitions, helping conveyancers identify common errors and improve application quality.

Can My Application Be Expedited?

Yes, sometimes. If a transaction is at risk (for example due to a mortgage offer expiring), you may qualify for a free expedite request. HMLR reports that most expedited applications are processed within 10 working days, provided all documentation is in order.

"*" indicates required fields

How to Help Avoid Delays

Instruct your solicitor early

Starting early allows your solicitor to prepare clean, complete documents.

Provide all requested information promptly

Errors or missing information are responsible for over 55% of registration delays.

Let your solicitor monitor the application

Prompt responses to any HMLR queries reduce the risk of the application being paused.

Ask whether your case qualifies for an expedite

We will always advise you if this is an option.

How Thornton Jones Solicitors Can Support You

Despite the ongoing registration delays, our experienced conveyancing team is here to:

- Submit accurate, complete applications to minimise requisitions

- Monitor progress and respond promptly to HMLR

- Advise on whether an expedite request is appropriate

- Guide you through the process with clear, timely updates

If you are concerned about a delayed registration, or want support with a new transaction, our team is ready to help.

For advice, assistance or to instruct us for your property sale or purchase please contact our team today on 01924 290 029 or via our online enquiry form.

Residential Conveyancing FAQs

HM Land Registry delays are mainly caused by high application volumes, increased complexity in modern property transactions, and ongoing system modernisation. Simple applications may still be processed relatively quickly, but more complex matters, such as transfers of part, new leases, and first registrations, are often taking many months due to backlogs and additional checks. If your transaction is being affected by delays, Thornton Jones Solicitors can help you minimise issues by ensuring your application is submitted correctly and proactively monitored throughout the process.

In 2026, typical HM Land Registry processing times vary depending on the type of application. Straightforward updates can take around 5–6 months, while more complex registrations may take 10–12 months or longer, with some cases extending beyond a year where further enquiries are required. For tailored advice on your property transaction or concerns about delays, Thornton Jones Solicitors can provide clear guidance and keep your matter progressing as efficiently as possible.

Yes. Delays can impact your ability to sell, remortgage, or prove legal ownership, particularly where the updated title register is required by lenders or buyers. Although your legal ownership is protected from the date HM Land Registry receives your application, practical issues can arise until registration is completed. If you are experiencing issues linked to delayed registration, Thornton Jones Solicitors can assist in progressing your application and advising on any risks to your transaction.

The content of this blog post is for information only and does not constitute formal legal advice and should not be relied upon as advice. Thornton Jones Solicitors Limited accepts no liability for any such reliance upon this content. Where the post includes links to external websites, Thornton Jones Solicitors Limited accepts no responsibility for the content of such sites. Any link to a third-party website should not be construed as endorsement by Thornton Jones Solicitors Limited of any content, products or services which are outside our direct control.

Residential Conveyancing Solicitors

Conveyancing Timeframes: Why Some Transactions Take 8 Weeks and Others Take 20+

Buying or selling a home is exciting but waiting for completion can be stressful. One of the most common questions we hear is: “How long will my conveyancing take?” The answer depends on several factors.

Conveyancing Timeframes: Type of Property

The type of property you are buying can have a big impact on the conveyancing process. Different property types come with their own legal considerations and potential complications, which can affect how long your transaction takes. Knowing what to expect for freehold, leasehold, new-build, or older and unusual properties can help you plan ahead and avoid unnecessary delays.

- Freehold vs Leasehold: Leasehold properties often need extra checks, like service charges and management approvals, which can add time.

- New Builds: Developers’ legal packs can speed things up or cause delays if incomplete.

- Older or unusual properties: Listed buildings or shared-access plots may require additional enquiries.

Conveyancing Timeframes: Mortgage and Searches

Obtaining a mortgage and carrying out property searches are key parts of the conveyancing process, but they can also impact how quickly a transaction progresses. Lenders require valuations, approvals, and supporting documentation, while local authority searches typically take 2–6 weeks and environmental searches typically take a few days. If any issues are uncovered, your solicitor will need to raise enquiries with the seller, which can add further time to your purchase.

- Lenders need valuations, approvals, and documentation, which can slow progress.

- Local authority searches typically take 2–6 weeks, depending on the council.

- Environmental searches typically take just a few days.

- If issues arise during searches, your solicitor will raise enquiries with the seller, which can add time.

Conveyancing Timeframes: Chains and Client Responsiveness

The length of a property chain can significantly influence how quickly a transaction completes. Short chains tend to move smoothly, while longer chains involving multiple buyers and sellers are more prone to delays. Your own responsiveness—providing signatures, proof of funds, and requested documents promptly—can make a real difference in keeping the process on track.

- Short chains move quickly, while long chains (multiple buyers and sellers) are more prone to delays.

- Responding promptly to requests for signatures, proof of funds, or documents helps speed things up.

If you are buying a property then you can use our FREE ONLINE CONVEYANCING CALCULATOR to get an instant and no-obligation online conveyancing quote. If you’d prefer to speak with a person, simply call us at any of our offices to speak to our expert residential conveyancing solicitors.

Conveyancing Timeframes: Unexpected Issues

Even straightforward transactions can hit surprises, such as:

- Title discrepancies

- Boundary disputes

- Conditional planning or restrictive covenants

Each may require extra investigation or negotiation.

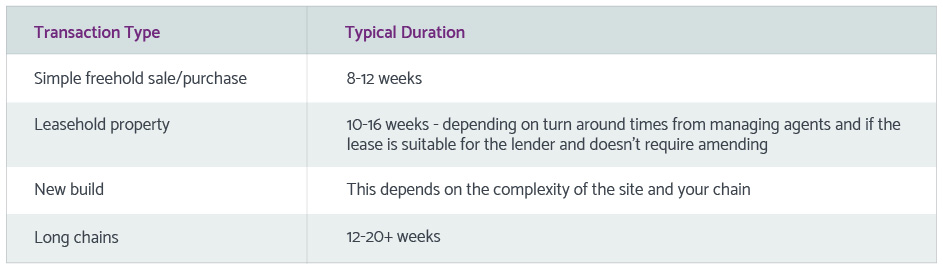

Typical Conveyancing Timeframes (guide only)

The table below outlines the typical conveyancing timeframes depending on the type of property transaction. A simple freehold sale or purchase usually takes between 8 and 12 weeks. Leasehold transactions tend to take longer, typically 10 to 16 weeks, as they often depend on managing agents’ turnaround times and whether the lease meets the lender’s requirements or needs to be amended.

New build purchases do not have a fixed timeframe, as the duration depends on the complexity of the development and the position of the property chain. Transactions involving long chains generally take the longest, often lasting 12 weeks or more, due to the additional coordination required between multiple parties.

How Thornton Jones Solicitors can Help with your Property Purchase

Our conveyancing team keeps you updated at every stage of the conveyancing process. We coordinate with mortgage lenders and other solicitors in the chain, and we proactively manages all enquiries to avoid unnecessary delays. Good communication is key to a smoother transaction.

Even though conveyancing times vary, understanding the factors at play can reduce stress and help you plan your move with confidence.

Whether you’re a first-time buyer or an experienced investor, we provide clear, proactive advice so you can move forward with confidence. Contact us today on 01924 290 029 or via our online enquiry form to speak with a solicitor who will handle your purchase efficiently and securely.

Conveyancing FAQs

Knowing the conveyancing process is crucial, whether you are a first-time buyer or a seasoned investor. The process typically involves three stages: pre-contract, exchange of contracts, and completion. Thornton Jones Solicitors recommend seeking professional guidance at each stage to ensure a smooth and legally secure transaction.

Conveyancing involves a lot of detailed work, yet fees are relatively low, making it a high-volume business. Delays often occur because solicitors are managing a large number of cases at once. Thornton Jones Solicitors advise keeping in regular contact with your conveyancer to stay updated throughout the process.

Delays can occur for various reasons, such as slow responses from buyers, sellers, or mortgage providers, or issues uncovered during searches. Thornton Jones Solicitors recommend proactive communication and early preparation to help minimise delays and keep your property transaction on track.

The content of this blog post is for information only and does not constitute formal legal advice and should not be relied upon as advice. Thornton Jones Solicitors Limited accepts no liability for any such reliance upon this content. Where the post includes links to external websites, Thornton Jones Solicitors Limited accepts no responsibility for the content of such sites. Any link to a third-party website should not be construed as endorsement by Thornton Jones Solicitors Limited of any content, products or services which are outside our direct control.

Contact our Conveyancing Solicitors in Garforth, Leeds

Thornton Jones Solicitors

Westbourne House

99 Lidgett Lane

Garforth

Leeds

LS25 1LJ

Tel: 0113 246 4423

Fax: 0113 831 4929

Email: enquiries@thorntonjones.co.uk

Contact our Conveyancing Solicitors in Wakefield

Thornton Jones Solicitors

Bank House

1 Burton Street

Wakefield

WF1 2GF

Tel: 01924 290029

Fax: 01924 290240

Email: enquiries@thorntonjones.co.uk

Contact our Conveyancing Solicitors in Ossett, Wakefield

Thornton Jones Solicitors

25 Bank Street

Ossett

WF5 8PS

Tel: 01924 586466

Fax: 01924 290240

Email: enquiries@thorntonjones.co.uk

Contact our Conveyancing Solicitors in Sherburn in Elmet, Leeds

Thornton Jones Solicitors

6 Finkle Hill

Sherburn in Elmet

Leeds

LS25 6EA

Tel: 01977 350500

Fax: 0113 831 4929

Email: enquiries@thorntonjones.co.uk

Why Do Conveyancing Clients Need to Provide ID?

In the process of buying or selling property, one of the first things we will ask for is proof of your identity. Requesting ID is not just standard practice, it’s a legal requirement that protects everyone involved in the transaction.

The primary reason ID is required is compliance with Anti-Money Laundering (AML) regulations. Law firms and conveyancers are legally obligated to verify the identity of their clients to prevent money laundering, fraud, and other criminal activities.

Why ID Checks Are Essential in Property Transactions

Buying or selling property is one of the most common ways illicit funds are “cleaned.” Criminals may attempt to use property transactions to legitimise money obtained through illegal means. To combat this, legal professionals must perform due diligence to ensure their clients are who they say they are and that the funds involved come from legitimate sources. Fraudsters can pose as property owners to illegally sell or mortgage a property they don’t own. This is especially common with vacant properties, tenanted properties, properties without a mortgage and elderly or vulnerable property owners.

The Legal Requirement for ID Checks in Property Transactions

By verifying your ID, conveyancers reduce the risk of fraudulent transactions. This protects not only their clients but also the integrity of the wider property market.

As part of their professional obligations, solicitors and conveyancers must carry out client due diligence, which includes verifying your identity, understanding the source of funds and assessing the nature of the transaction.

Without proper ID verification we cannot proceed with your matter — not only because it would be a breach of regulation, but because it could potentially facilitate criminal activity.

For all parties involved, ID verification adds transparency to the process. It’s a reassurance that everyone involved is genuine, and that the transaction is being conducted properly.

Typically, the ID you will need to provide are:

- one form of photographic ID (eg Passport or Driving Licence)

- one proof of address (eg utility bill, bank statement, council tax bill — dated within the last 3 months).

These can all be provided via an electronic ID verification app which is simple and easy to use.

Providing ID might feel like a formality, but it plays a vital role in protecting you, your property, and the entire conveyancing process. These checks are not designed to make things difficult — they are there to ensure that property transactions are secure, transparent, and compliant with the law.

Contact us for Residential Conveyancing Advice

Need expert guidance on your property transaction? Contact our residential conveyancing team today for personalised advice on 01924 290 029, or contact us using our online enquiry form.

Residential Conveyancing FAQs

Solicitors must check your identity to comply with Anti-Money Laundering (AML) regulations. This helps prevent fraud, money laundering, and protects all parties in a property transaction.

Typically, you’ll need a government-issued photo ID (like a passport or driving licence) and proof of address (such as a utility bill or bank statement). Your solicitor will confirm the exact requirements.

No. ID verification is a legal requirement. Delaying it can slow down your property transaction and may even prevent the sale or purchase from completing.

Most ID checks are quick and can be completed within a day if you provide the required documents promptly. Delays usually occur if documents are missing, unclear, or need further verification.

Yes. Under UK law, all conveyancing transactions must include identity verification to comply with Anti-Money Laundering regulations, regardless of property type or value.

Your solicitor may request additional documents or refuse to proceed until compliant ID is provided. Using outdated or incorrect documents can delay the transaction or create legal complications.

The content of this blog post is for information only and does not constitute formal legal advice and should not be relied upon as advice. Thornton Jones Solicitors Limited accepts no liability for any such reliance upon this content. Where the post includes links to external websites, Thornton Jones Solicitors Limited accepts no responsibility for the content of such sites. Any link to a third-party website should not be construed as endorsement by Thornton Jones Solicitors Limited of any content, products or services which are outside our direct control.

Contact our Residential Conveyancing Solicitors in Garforth, Leeds

Thornton Jones Solicitors

Westbourne House

99 Lidgett Lane

Garforth

Leeds

LS25 1LJ

Tel: 0113 246 4423

Fax: 0113 831 4929

Email: enquiries@thorntonjones.co.uk

Contact our Residential Conveyancing Solicitors in Wakefield

Thornton Jones Solicitors

Bank House

1 Burton Street

Wakefield

WF1 2GF

Tel: 01924 290029

Fax: 01924 290240

Email: enquiries@thorntonjones.co.uk

Contact our Residential Conveyancing Solicitors in Ossett, Wakefield

Thornton Jones Solicitors

25 Bank Street

Ossett

WF5 8PS

Tel: 01924 586466

Fax: 01924 290240

Email: enquiries@thorntonjones.co.uk

Contact our Residential Conveyancing Solicitors in Sherburn in Elmet, Leeds

Thornton Jones Solicitors

6 Finkle Hill

Sherburn in Elmet

Leeds

LS25 6EA

Tel: 01977 350500

Fax: 0113 831 4929

Email: enquiries@thorntonjones.co.uk

What the 2025 Budget “Mansion Tax” Means for Homeowners

In the Autumn 2025 Budget, Chancellor Rachel Reeves announced a new property tax coined “mansion tax” (officially the High Value Council Tax Surcharge, or HVCTS) targeting high-value homes. This will have important legal implications for property owners, buyers and sellers.

What is the new Mansion Tax introduced in the 2025 Budget?

The 2025 Budget introduced a new property tax, officially called the High Value Council Tax Surcharge (HVCTS), often referred to as the “mansion tax.” It targets residential properties in England valued over £2 million, adding an annual levy on top of standard council tax. The surcharge is designed to make high-value homeowners contribute more fairly to public finances and will take effect from April 2028.

Who will the new Mansion Tax surcharge affect?

The surcharge will apply to residential properties in England valued at more than £2 million (based on valuations set in 2026) and will take effect from April 2028. Affected homeowners will pay an annual levy, in addition to their existing council tax.

The surcharge is structured in four bands:

- For properties valued at £2 million to £2.5 million the additional charge will be £2,500 per annum.

- For properties valued at £2.5 million to £3.5 million the additional charge will be £3,500 per annum.

- For properties valued at £3.5 million to £5 million the additional charge will be £5,000 per annum.

- For properties valued at over £5 million the additional charge will be £7,500.00 per annum.

What are the potential future changes to the Mansion Tax?

After initial implementation, the surcharge amounts will be adjusted annually by CPI (Consumer Price Index) inflation. Thresholds will thereafter be reviewed every five years. It is important to note that the surcharge is payable by the owner, not necessarily the occupier. Therefore, if you rent a property worth in excess of £2million the tax is payable by the homeowner and not the tenant. However, we may see rents increasing to cover the homeowner’s costs.

What is the aim of the Mansion Tax?

In her Budget statement, Rachel Reeves maintained the surcharge is intended to correct a longstanding imbalance. Arguing that under the current system, many high-value homes (including multimillion-pound properties) often pay comparable council tax to similar houses in less affluent areas.

The aim of the tax is to ensure that owners of high-value properties contribute more fairly to public finances in part of a broader push to address wealth inequality and make the tax system more progressive.

For many top-end homeowners, this will represent a significant annual cost increase.

What are the implications of the Mansion Tax?

There are several implications which may require planning and advice:

- For Current Owners of High-Value Homes: owners of homes valued above £2 million must budget for the extra annual surcharge from 2028.

- For “asset-rich but cash-poor” owners (e.g. retirees who own expensive properties but have modest income) the surcharge could present a real financial burden. It’s worth reviewing long-term financial plans (e.g. pension income, ability to pay) now, especially where properties may have increased in value significantly since purchase.

- For Those Buying or Selling in the High-Value Market: because the surcharge is based on 2026 valuations, the value band a property falls into may shift by the time the surcharge begins. Buyers and sellers should factor in potential future liability when negotiating price or structuring deals. Some buyers may be deterred by the surcharge, which could affect demand, this is of particular concern for properties around the £2–3 million mark. Sellers should be aware that prospective buyers may renegotiate to offset the future annual surcharge.

- For Estate Planning & Inheritance/Wealth Structuring: for clients with high-value properties, especially those considering inheritance planning, trusts, or long-term housing arrangements, the surcharge adds another dimension to wealth management.

The surcharge will be based on 2026 valuations by the Valuation Office Agency (VOA), and valuations for some high-value homes may be contentious which will lead to valuation appeals. This will inevitably create administrative backlog and uncertainty.

For some homeowners, especially those who bought decades ago, historic valuations may underestimate the current market value meaning unexpected jumps into higher surcharge bands.

The surcharge could distort the high-end property market over time: potential reduction in demand, properties being sold off, “value-bunching” just below the threshold which could create disputes in transactions or valuations.

Why It Matters — And Why Legal Advice Is Crucial

The introduction of the high-value surcharge reflects a major shift in UK property taxation. While the surcharge will only affect a minority of homes (less than the top 1% by value), the financial and legal consequences for those homeowners are substantial.

For existing homeowners, prospective buyers, and estate planners alike, understanding the surcharge, and planning accordingly, is vital. If you own (or are considering purchasing) a high-value property now is the time to consider whether you should take professional legal and financial advice.

Our Final Thoughts on the Mansion Tax

The 2025 “mansion tax” is more than a headline. It is a structural change to how high-value homes are taxed. For those homeowners affected, it may mean significant extra costs and a re-evaluation of long-term property plans. For buyers and sellers, it may influence property values and negotiation strategies

Mansion Tax FAQs

The surcharge applies to residential properties in England valued over £2 million based on 2026 valuations. Homeowners (not tenants) are responsible for paying the annual levy, which ranges from £2,500 to £7,500 depending on property value.

Thornton Jones Solicitors advise that homeowners start reviewing their finances now to prepare for the additional costs.

The High Value Council Tax Surcharge will take effect from April 2028. The tax bands are based on 2026 property valuations, and annual amounts will be adjusted for inflation.

Thornton Jones Solicitors suggest marking this date in your planning calendar and considering professional legal or financial advice well in advance.

Buyers and sellers may need to factor in the surcharge when negotiating property prices, especially for homes around £2–3 million. Estate planning could also be affected, as the surcharge adds costs for inheritance, trusts, and long-term housing arrangements.

Thornton Jones Solicitors advise consulting a legal professional to assess the potential impact on property transactions and wealth planning.

The content of this blog post is for information only and does not constitute formal legal advice and should not be relied upon as advice. Thornton Jones Solicitors Limited accepts no liability for any such reliance upon this content. Where the post includes links to external websites, Thornton Jones Solicitors Limited accepts no responsibility for the content of such sites. Any link to a third-party website should not be construed as endorsement by Thornton Jones Solicitors Limited of any content, products or services which are outside our direct control.

Why Do Conveyancers Require Proof of Source of Funds?

When purchasing a property, your conveyancer will request proof of the source of your funds. While this may initially seem unnecessary, it is in fact a legal requirement and an essential safeguard in the conveyancing process. Establishing the legitimacy of monies used in a property purchase protects clients, conveyancers, and the wider property market.

What does “Source of Funds” mean in Conveyancing?

The term “source of funds” refers to the origin of the money being used to buy a property. This may include:

- Personal savings built up over time;

- Proceeds from the sale of another property or asset;

- An inheritance from an estate;

- Investment or dividend income;

- A financial gift from a family member;

- A mortgage advance from a lender.

Conveyancers are required to obtain documentation to verify these funds. Examples include bank statements, inheritance paperwork, property completion statements, or formal gift letters.

If you are buying a property then you can use our FREE ONLINE CONVEYANCING CALCULATOR to get an instant and no-obligation online conveyancing quote. If you’d prefer to speak with a person, simply call us at any of our offices to speak to our expert residential conveyancing solicitors.

Why do conveyancers ask for proof of source of funds?

1. Compliance with Anti-Money Laundering Regulations

Solicitors are bound by strict Anti-Money Laundering (AML) legislation. Property transactions are sometimes exploited by criminals seeking to “clean” illicit funds. By conducting thorough source of funds checks, conveyancers ensure compliance with AML regulations and uphold the integrity of the property market.

2. Protecting property buyers

Verifying funds is also in the best interests of the purchaser. If money used in a property transaction is later linked to criminal activity, authorities may have the right to seize the property, even if the buyer was unaware. Proper AML checks during conveyancing help safeguard your investment.

3. Preventing delays and transactional risks

If satisfactory evidence of funds is not provided, the conveyancing process may be delayed or, in some cases, the transaction could collapse. Supplying clear documentation at the outset ensures a smoother and more efficient property purchase.

What documents may be required as proof of source of funds?

Depending on your individual circumstances, your conveyancer may ask for:

- Recent bank statements showing the accumulation of savings;

- A grant of probate or executor’s letter confirming inheritance;

- A completion statement from the sale of another property;

- Statements from investments or shareholdings;

- A signed gift letter and supporting bank statements from the donor.

How clients can support the process

To assist your conveyancer in completing the necessary checks:

- Be open and transparent regarding the source of your funds;

- Provide documentation promptly when requested;

- Avoid unnecessary transfers between accounts, which complicate the audit trail;

- Retain copies of all relevant paperwork.

What to Expect in the Initial Stages of a Conveyancing Transaction

There are many steps involved in the initial stage (which we often call the initial instructions) of conveyancing. In this blog by Jemima Abbey-smith, we attempt to break them down into easy-to-understand and digestible steps.

Conclusion

Providing proof of source of funds is a crucial part of any property purchase. While it may feel burdensome, these checks are in place to comply with anti-money laundering regulations, protect property buyers, and ensure a secure transaction.

If you are preparing to purchase a property and require advice on evidencing your funds, our experienced conveyancers are here to guide you through every stage of the process with clarity and professionalism.

Ensure your property purchase runs smoothly. Contact our specialist Residential Conveyancing solicitors in Yorkshire.

If you are preparing to buy a property and need advice on evidencing your source of funds, our experienced conveyancing team can guide you through the process. We provide clear, practical advice to help you meet legal requirements and avoid unnecessary delays.

Speak to our expert residential conveyancing solicitors in Wakefield, Ossett, Garforth, and Sherburn in Elmet, Yorkshire today by calling 01924 290 029 or ask a question using our online enquiry form.

The content of this blog post is for information only and does not constitute formal legal advice and should not be relied upon as advice. Thornton Jones Solicitors Limited accepts no liability for any such reliance upon this content. Where the post includes links to external websites, Thornton Jones Solicitors Limited accepts no responsibility for the content of such s

Proof of Source of Funds FAQs

The “source of funds” refers to the origin of the money used to buy a property. This could include savings, proceeds from selling another property, inheritance, investments, or a financial gift. Conveyancers need this information to verify the legitimacy of the funds.

Conveyancers are required by Anti-Money Laundering (AML) regulations to confirm that property funds are legitimate. Verifying your funds protects you, your solicitor, and the property market from potential financial crime.

Depending on your situation, you may need to provide bank statements, inheritance paperwork, property sale completion statements, investment records, or signed gift letters from family members.

The verification process varies but is usually completed quickly if you provide clear, organised documentation. Delays often occur when paperwork is missing, unclear, or requires additional explanation.

If sufficient evidence isn’t supplied, the conveyancing process may be delayed or, in some cases, the property purchase could fail. Providing full and transparent documentation ensures a smoother, legally compliant transaction.

What is Adverse Possession?

Adverse possession is a legal principle whereby someone can claim ownership and have land registered to themselves at Land Registry on the basis of occupying the land for a certain period of time.

Adverse possession is sometimes referred to as “squatters’ rights”, but it applies in a range of situations beyond abandoned buildings. It can arise where boundaries are disputed, land has been enclosed or maintained without permission, or where the legal owner has not used or monitored the land for many years. The law is designed to balance the rights of property owners with those who have made long-term, exclusive use of land.

How do I make an Adverse Possession claim?

A claim for adverse possession is made by submitting an application to Land Registry in the format of an ADV1 form, along with a sworn declaration setting out the history and details of the use of the land in question, along with any other available evidence to support the application.

If Land Registry are satisfied their requirements are met, they will then serve notice of the pending application on the owner of the land to make them aware of the intended registration. If the Land is unregistered, Land Registry will serve notice on anyone who may have a potential interest in the land i.e. potential owners and neighbouring properties.

The registered owner or interested party will have a period of 65 days from receipt of the notice to respond. The options for the registered owner are as follows:

- Object to the application – If the owner or an interested party objects to the application then the Land Registry will notify the applicant and the matter can be referred to the Land Registry Dispute Resolution Process to attempt to resolve the conflict.

- Serve a Counter Notice – The owner or interested party can serve a Counter Notice which prevents the Land Registry from completing the registration without further investigation. If a Counter Notice is served, the applicant has to attempt to prove they meet the requirements for the application to be accepted.

- Do nothing/accept the application – If the 65 days pass and no correspondence has been received from the land owner, or they acknowledge and confirm they have no objections to the application then Land Registry will accept the application and register the land to the applicant with Possessory Title.

What is a Possessory Title?

A Possessory Title is a lesser class of Title whereby the owner does not have full legal proof of ownership of the land and there may be ambiguity over the ownership. Once a period of 12 years has passed, Land Registry will be willing to upgrade to Absolute Title which gives unequivocal rights of ownership.

What are the requirements for an Adverse Possession claim?

In order to be able to make a successful claim the applicant must be able to illustrate the following within their application:

- Factual Possession of the land – The applicant must be able to show they have treated the land as their own and have had control of the same e.g. enclosing the land with fencing.

- The intention to possess – The applicant must show more just the factual possession, but also their intention in possessing the land as their own and to exclude the legal owner e.g. making improvements and maintaining the land.

- Adverse possession – The applicant must be able to show that the possession has been without the legal owners consent i.e. there have been no discussions or agreement as to the use and that there are no permissions in place to do so.

What is the time period required to make an Adverse Possession claim?

- If the land is registered, the applicant must be able to provide evidence of 10 years of use.

- If the land is unregistered, the applicant must be able to provide evidence of 12 years of use.

- The period of use must have been continuous and uninterrupted.

Contact our specialist residential conveyancing team in Yorkshire

If you think you may have a potential claim for adverse possession or require further advice in relation to adverse possession then our specialist residential conveyancing team will be able to assist. Find out more about how we can help you by calling any of our offices to arrange an appointment.

Speak to our expert residential conveyancing solicitors in Wakefield, Ossett, Garforth, and Sherburn in Elmet, Yorkshire today by calling 01924 290 029 or ask a question using our online enquiry form.

The content of this blog post is for information only and does not constitute formal legal advice and should not be relied upon as advice. Thornton Jones Solicitors Limited accepts no liability for any such reliance upon this content. Where the post includes links to external websites, Thornton Jones Solicitors Limited accepts no responsibility for the content of such sites. Any link to a third-party website should not be construed as endorsement by Thornton Jones Solicitors Limited of any content, products or services which are outside our direct control.

Adverse possession, sometimes called squatters’ rights, is when someone occupies land without the owner’s permission and may gain legal ownership after meeting strict legal requirements.

In England and Wales, you usually need 10 years of continuous possession for registered land, or 12 years for unregistered land, to apply for ownership.

Yes. The landowner can object or serve a counter notice within 65 business days of being notified by Land Registry, which can block or delay the claim.

Fencing is strong evidence of factual possession, but maintaining, cultivating, or otherwise excluding others from the land can also support a claim.

If successful, you’ll usually be registered with Possessory Title. This can be upgraded to Absolute Title after 12 years if there are no legal disputes.

What’s the difference between Freehold, Leasehold & Commonhold?

When buying a property, you will often come across the terms freehold, leasehold and commonhold – but what do these mean? It is important to learn the difference between these types of property ownership as they each have their own pros and cons. It is up to you to decide what is the most suitable for your lifestyle and budget.

What is a Freehold property?

Freehold is the most common and complete type of property ownership. If you own a freehold property this means you own both the building and the land it stands on outright. There is also no time limit on freehold properties, your ownership is permanent until you decide to sell. As you own the whole of the property and the land, you are responsible for maintaining everything, including any garden or driveway.

What is a Leasehold property?

Leasehold is the most common type of property ownership for flats and apartments, but there are leasehold houses as well. Owning the leasehold gives you the right to use a property for a set period of time as outlined in the lease agreement with the freeholder (also known as the landlord). As the owner of the leasehold, you own the property for the duration of the lease, which can range from a few years to 999 years. Unlike owning a freehold property, if you own a leasehold property, you do not own the land that the property is built on, this is owned by the freeholder/landlord.

As you do not own the land the property is built on, you are usually required to pay ground rent, service charges, and maintenance fees to the freeholder. These payments are usually sent to a management company who act on behalf of the freeholder. Similar to when renting a property, you will need permission from the freeholder to make any major changes to the property. You may also need permission to have any pets and if you plan on running a business from home. One other thing to note about owning a leasehold property is that the landlord is responsible for the maintenance of the land. This also includes any shared areas such as communal gardens and hallways.

How much time remains on the lease?

Lease terms can differ significantly, though most new leases are granted for between 99 and 125 years, with some extending up to 999 years. If you’re purchasing a leasehold property, it’s essential to check how much time is left on the lease, particularly if it’s not newly granted. Leases with fewer than 80 years remaining may impact your ability to secure a mortgage. Additionally, you typically need to have owned the property for at least two years before you’re eligible to apply for a lease extension.

"*" indicates required fields

What is a Commonhold property?

Commonhold is the rarest type of property ownership. It was introduced by the Commonhold and Leasehold Reform Act 2002 as an alternative to leasehold ownership, particularly for flats and other properties with shared areas. Unlike leasehold, commonhold means you own the property outright and forever, not just for a set period of time. Shared areas such as hallways, gardens and roofs are owned and managed collectively by the ‘Commonhold Association’, which is a company made up of all the unit owners. This means that decisions about the maintenance, rules and costs of the shared areas are made by the owners/residents, rather than a separate landlord or management company.

Yes, in many cases leaseholders have the right to buy the freehold of their property through a process known as “freehold enfranchisement.” The rules vary depending on whether the property is a house or a flat.

When a lease expires, ownership of the property typically reverts to the freeholder. It’s important to consider lease length when buying, as a short lease can significantly affect the property’s value and the ability to secure a mortgage.

Commonhold can offer more autonomy and transparency than leasehold, especially for flat owners, as there is no landlord and decisions are made collectively. However, it’s still relatively rare, so support and infrastructure for commonhold properties can be limited.

Yes, leaseholders usually need permission from the freeholder to make structural alterations, keep pets, or run a business from home. The exact restrictions will be detailed in the lease.

What Is the New Commonhold Model for Homeownership in England and Wales?

The Government has recently announced plans to reinvigorate commonhold and bring the current leasehold system to an end. They have proposed a ban on the granting of new leasehold houses (with some exceptions), as well as making it cheaper and easier for leaseholders to extend their lease or buy the freehold of their property. They also want to reduce ground rent to a peppercorn (meaning a very low or minimal amount), as well as improve the transparency on how service charges are spent.

These changes are in an effort to prevent landlords and management companies from charging unreasonable costs, and subjecting homeowners to unfair living conditions. The Government wish to empower leaseholders by giving them more rights and security, so that homeowners will have a greater say in how their home is managed and the bills they pay, rather than third-party landlords.

At time of writing we cannot yet say when, or indeed if, these reforms will come into effect. But the Leasehold and Freehold Reform Act 2024 received a Royal assent on the 24th of May 2024, and the Government has stated that they are committed to implement the Act ‘as quickly as possible’.

The Leasehold and Freehold Reform Act 2025

Find out more about the Leasehold and Freehold Reform Act 2025 including the latest news coming from the Government on the matter by clicking here.

How can we help?

If you are buying a property, whether it be freehold, leasehold, or commonhold, our specialist Residential Conveyancing Team can help. We can assist you in navigating the intricacies of the matter ensuring that you fully understand the detail of the transaction before proceeding.

We will guide you through each step of the conveyancing process, from reviewing title deeds and lease terms to explaining your rights and responsibilities as a property owner. Our goal is to ensure that you feel confident in your decision and protected throughout the purchase.

Find out more about how we can help you with your property purchase by calling our team at any of our offices or, for a no-obligation conveyancing quote use our online conveyancing quote tool.

The content of this blog post is for information only and does not constitute formal legal advice and should not be relied upon as advice. Thornton Jones Solicitors Limited accepts no liability for any such reliance upon this content. Where the post includes links to external websites, Thornton Jones Solicitors Limited accepts no responsibility for the content of such sites. Any link to a third-party website should not be construed as endorsement by Thornton Jones Solicitors Limited of any content, products or services which are outside our direct control.

Stamp Duty Land Tax Changes in April 2025

Stamp Duty Land Tax (SDLT) is a key part of the property purchasing process in the UK. For many buyers, it can be a significant cost to factor in when buying a property. Recent changes to SDLT have made headlines, and new requirements were rolled out on 1st April 2025.

What is SDLT?

Stamp Duty Land Tax, often referred to as just Stamp Duty, is a tax levied on the purchase price of property or land in England, Wales, and Northern Ireland. The amount of Stamp Duty owed is based on the value of the property or land being purchased. The tax is paid by the buyer, and the amount depends on whether the property is residential or non-residential, as well as the buyer’s status, for example a first-time buyer or a buy-to-let investor.

What are the Stamp Duty Land Tax Changes?

The new Stamp Duty rules and thresholds were introduced on 1st April 2025 and they are as follow:

1. First Time Buyer Relief:

What is the First-Time Buyer Stamp Duty Relief?

For first-time buyers, the Stamp Duty Land Tax threshold has been raised. If you are a first-time buyer purchasing a property for less than £500,000, you may be eligible for relief. You won’t pay Stamp Duty on properties valued up to £300,000. For properties priced between £300,001 and £500,000, a reduced rate of 5% will apply on the portion of the price above £300,000. However, first-time buyer relief is not available for properties over £500,000. It’s important to note also that you will not qualify for the First Time Buyers Relief if you purchase a property jointly with someone who is not a first time buyer.

2. Buy-To-Let Properties:

Is Stamp Duty payable on Buy-to-Let Properties?

Prior to the 1st April 2025 changes to SDLT, individuals purchasing buy-to-let properties or second homes faced a 3% surcharge on top of the standard SDLT rates. While this surcharge remains, there have been adjustments to the thresholds at which the different SDLT rates apply meaning more Stamp Duty will now be payable. The new thresholds are as follows:

Stamp Duty Thresholds for Residential Properties:

- Up to £125,000: No Stamp Duty payable

- Between £125,001 to £250,000: 2%

- Between £250,001 to £925,000: 5%

- Between £925,001 to £1,500,000: 10%

- Above £1,500,000: 12%

Stamp Duty Thresholds for First-Time Buyers:

- Up to £300,000: 0%

- £300,001 to £500,000: 5%

- £500,001: No relief available

Therefore, for a buy-to-let purchase or a purchase that is a second home, the above rates apply plus the additional 3% surcharge.

3. Non-UK Residents:

What is the Stamp Duty surcharge for Non-UK Residents?

The government has introduced additional measures for non-UK residents who purchase a property in England and Northern Ireland. There will now be a 2% surcharge on properties purchased by individuals who are non-UK residents.

4. Higher-Value Properties:

What are the Higher Rates of Stamp Duty for Higher-Value Properties?

Another significant change that has taken place is the increase in SDLT rates for more expensive properties. For properties priced over £1.5 million, the tax rate on the portion above £1.5 million is now set at 12%.

Blog: What to Expect in the Initial Stages of a Conveyancing Transaction

There are many steps involved in the initial stage (which we often call the initial instructions) of conveyancing. Here we attempt to break them down into easy-to-understand and digestible steps.

A blog by Jemima Abbey-Smith

How Do the New Stamp Duty Rates Affect Buyers?

The new rates which came into effect on 1st April 2025 see an increase in the amount of Stamp Duty payable. The new rates are:

Stamp Duty Thresholds for Residential Properties:

- Up to £125,000: No Stamp Duty payable

- Between £125,001 to £250,000: 2%

- Between £250,001 to £925,000: 5%

- Between £925,001 to £1,500,000: 10%

- Above £1,500,000: 12%

Stamp Duty Thresholds for First-Time Buyers:

- Up to £300,000: 0%

- £300,001 to £500,000: 5%

- £500,001: No relief available

The amount of Stamp Duty owed (also known as Stamp Duty Land Tax) is determined by the purchase price of the property or land. These thresholds can change so it’s advisable to discuss your specific situation with a conveyancing solicitor who will provide you with the most up-do-date information. The latest Stamp Duty Thresholds are available on www.gov.uk.

You are considered a first-time buyer if you are purchasing a property that will be your only or main residence, and you have never owned a freehold or have a leasehold interest in a residential property in the UK or abroad. Note also that if you’ve ever inherited a property (or part of one), you won’t be considered a first-time buyer.

To pay the Stamp Duty owed you will need to complete a Stamp Duty Land Tax (SDLT) Return and pay the required amount of SDLT due. You must submit the return and pay the tax within 14 days of completion otherwise HMRC might charge you penalties and interest. Usually your conveyancing solicitor will complete this on your behalf. Your conveyancing solicitor will be able to complete this online however if you are doing tis yourself as an individual then you will be required to complete and submit a paper form.

The New Stamp Duty Land Tax Thresholds: In summary

As a buyer, it’s essential to stay up to date with these changes and understand how they affect your purchasing power. Inevitably, purchasers will now be required to pay more for their SDLT liability. By working with the right professionals such as the Thornton Jones Solicitors conveyancing team in your property purchase and planning ahead, you can navigate the Stamp Duty landscape smoothly and ensure your property transaction is as cost-effective as possible.

Find out more about how we can help you with your conveyancing, including calculating your Stamp Duty liability, by calling our team at any of our offices or, for a no-obligation conveyancing quote use our online conveyancing quote tool.

The content of this blog post is for information only and does not constitute formal legal advice and should not be relied upon as advice. Thornton Jones Solicitors Limited accepts no liability for any such reliance upon this content. Where the post includes links to external websites, Thornton Jones Solicitors Limited accepts no responsibility for the content of such sites. Any link to a third-party website should not be construed as endorsement by Thornton Jones Solicitors Limited of any content, products or services which are outside our direct